Table of Contents >> Show >> Hide

- Why Everyone Is Waiting for a Housing Price Crash

- What History Actually Says About Home Price Drops

- What the Latest Forecasts Say (Spoiler: Drip, Not Crash)

- The Big Forces That Decide If Prices Actually Fall

- So… When Might Home Prices Actually Go Down?

- What “A Wealth of Common Sense” Can Teach Us

- Practical Moves for Buyers, Sellers, and Homeowners

- Real-World Experiences with Waiting for Prices to Fall

If you’ve asked yourself, “When will housing prices finally fall?” you’re in good company. Buyers are exhausted, sellers are confused, and homeowners are doom-scrolling charts of mortgage rates the way they used to scroll vacation photos. Everyone seems to be waiting for the big housing crash that makes real estate “affordable again.”

Here’s the catch: the housing market doesn’t follow our feelings. It follows math, demographics, supply, and interest rates. And if you look at the actual data instead of viral headlines, a more boring (and more realistic) story appears: instead of a dramatic crash, the United States is far more likely to see slow, uneven adjustments in home prices over the next few years.

Think of this as a common-sense guide to the question of when home prices might fall, what history tells us, what experts are forecasting, and how to make smart decisions even when the market doesn’t do what you want it to.

Why Everyone Is Waiting for a Housing Price Crash

The last few years turned the housing market into a roller coaster. Home prices surged during the pandemic as:

- Mortgage rates plunged below 3%.

- Buyers looked for more space to work and live.

- Builders struggled with labor and material shortages.

Then inflation spiked, the Federal Reserve hiked interest rates aggressively, and 30-year mortgage rates jumped into the 7% range. Affordability got crushed. For many would-be buyers, the monthly payment on a typical home suddenly looked more like a luxury car lease… plus a small second car.

That’s why so many people assume a big price drop has to be coming. The logic sounds simple: if houses got too expensive, surely prices must fall. But housing is not like a stock that can be traded in milliseconds by millions of investors. It’s a slow, sticky market shaped by people who need a place to live and owners who don’t have to sell.

What History Actually Says About Home Price Drops

National home prices rarely fall in a big way

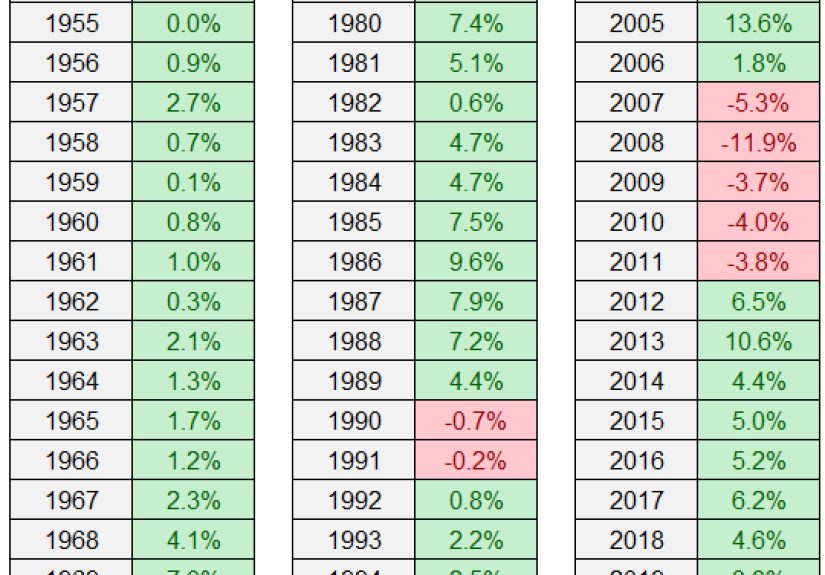

One of the most useful things about the “A Wealth of Common Sense” perspective is that it focuses on long-term data instead of emotions. When you look at national home price indexes over multiple decades, something surprising jumps out: big, sustained nationwide price declines are extremely rare.

Since the early 1990s, the United States has had exactly one massive national housing bust: the 2007–2011 period tied to the subprime mortgage crisis. In those years, home prices dropped sharply in many markets, wiping out equity and leaving millions underwater. Outside of that episode, the national trend has been pretty steady: prices might flatten, grow slowly, or dip a bit in specific regions, but they usually don’t collapse across the entire country all at once.

Recent data supports that pattern. National home price indexes show that by late 2025, U.S. home prices are still slightly higher than a year earlier, even though the pace of growth has cooled dramatically. In other words, price growth has slowed, but broad-based national price declines remain the exception, not the rule.

Local corrections are far more common than national crashes

While the national numbers might look calm, the view on the ground is much more chaotic. Some markets that overheated during the pandemic have already seen mild price pullbacks. Others, especially in the Midwest and parts of the Northeast, are still posting modest gains. A few states and metro areas have even started to see month-over-month declines while others continue inching up.

This is the first big common-sense lesson: asking “When will housing prices fall?” is like asking “When will the weather get cold?” The answer depends on where you are. Boise is not Boston, Phoenix is not Pittsburgh, and Miami is definitely not Milwaukee. Instead of a single national “crash date,” it’s much more realistic to expect multi-speed markets where some places correct, some plateau, and some keep climbing slowly.

What the Latest Forecasts Say (Spoiler: Drip, Not Crash)

Economists, real estate data firms, and mortgage agencies are constantly updating their home price forecasts. While their exact numbers differ, the broad message heading into 2026 is surprisingly consistent: modest growth, not a huge fall.

- Several major housing forecasts expect U.S. home prices to rise roughly 1–3% per year over the next few years, slower than recent history but still positive.

- Some research points to very small year-over-year gains nationally, with certain markets seeing slight declines and others modest increases.

- Mortgage and housing agencies that track home price indices are generally projecting cooling growth, not a full-on reversal.

In plain English: the expert consensus right now leans toward a “soft landing” where price growth slows and the market gradually rebalances, rather than a dramatic crash where homes suddenly become cheap.

Could those forecasts be wrong? Of course. Housing models can’t predict every shock. But from a common-sense standpoint, it’s helpful to recognize that the people who stare at this data all day long are mostly expecting a slow drip, not a waterfall.

The Big Forces That Decide If Prices Actually Fall

So what would it take for home prices to actually fall in a noticeable way? Four big forces matter most: mortgage rates, supply, demand (especially demographics), and the broader economy.

1. Mortgage rates: the on/off switch for demand

Mortgage rates are the single most powerful short-term lever in the housing market. When rates are low, the same monthly budget can support a much higher home price. When rates rise, that purchasing power disappears.

Right now, many forecasts suggest that mortgage rates may drift lower over the next couple of years, but not back to the ultra-cheap levels of 2020–2021. Think something in the mid–5% to low–6% range rather than 2–3%. That’s better than recent peaks but still high enough to keep some buyers on the sidelines.

Lower rates generally support prices by bringing more buyers back into the market. For a broad national price decline, you’d typically need the opposite: higher rates that severely limit affordability, combined with other negative forces like rising unemployment.

2. Supply: years of underbuilding still matter

Even with demand cooling, the U.S. has a structural supply problem. After the Great Financial Crisis, homebuilding lagged household formation for years. Many markets never fully caught up. Zoning rules, labor shortages, and high material costs continue to restrict building in some high-demand areas.

This chronic underbuilding acts like a floor under prices. If a city has more people who need homes than homes available, sellers don’t have to slash prices dramatically; they just wait for the right buyer. Unless construction meaningfully outpaces demand for a while, a sharp, sustained national price decline is hard to sustain.

3. Demographics: millennials and Gen Z are still coming

Demographics don’t move quickly, but they’re powerful. Millennials are in their peak homebuying years, and Gen Z is right behind them. Even if some choose to rent longer due to high prices and rates, the basic desire for stable housing doesn’t vanish.

This large wave of potential buyers puts steady pressure on the housing stock. That doesn’t mean millennials are thrilled about current prices (they’re not), but it does mean there’s a strong underlying demand base that keeps the market from collapsing unless something else goes seriously wrong.

4. Jobs and recessions: the wild card

Employment is the quiet backbone of the housing market. As long as most people have jobs and incomes are growing (even slowly), most homeowners can keep making their mortgage payments. They might not like their rate, but they can afford their home.

Many housing economists have noted that the last big housing crash was tied not just to bad lending, but to a brutal recession and rising unemployment. Some experts have argued that substantial national price declines are unlikely without a significant downturn in the job market. That’s why housing outlooks often come packaged with broader economic forecasts: if the economy slows but doesn’t break, home prices may flatten or inch down in spots, not collapse.

So… When Might Home Prices Actually Go Down?

Here’s the honest answer: there is no calendar date circled in red when U.S. home prices will automatically fall. Instead, think in terms of scenarios and probabilities.

Scenario 1: “Prices fall” in real terms, not on paper

One of the most likely paths is that home prices don’t drop dramatically in dollar termsbut inflation and wage growth slowly catch up. If nominal prices grow 1–2% per year while incomes rise faster, homes gradually become more affordable even though the sticker price never actually goes down.

From a buyer’s perspective, this feels like a long, frustrating wait. From a macro perspective, it’s a gentle way for the market to correct without a crash.

Scenario 2: Mild national dip, bigger local declines

Another realistic scenario: a modest national decline of a few percent over a year or two, with much larger declines in specific overheated markets. Some states and metro areas already show small price dips while others hold up or continue to rise slightly.

If unemployment were to rise or rates stayed higher for longer than expected, this kind of mild national drop paired with sharper local corrections becomes more likely. Even then, it’s more “ouch” than “apocalypse.”

Scenario 3: The crash everyone keeps tweeting about

The big dramatic crash think 20–30% national price declines would probably require a combination of nasty ingredients: a deep recession, high and sticky unemployment, financial stress, and forced selling by a large number of homeowners or investors. That’s possible, but it is not the base-case scenario most mainstream forecasters are using right now.

Common sense takeaway: the market can absolutely move against you, but building your life around the hope of a once-in-a-generation crash is risky. You may wait years… and watch prices grind sideways or up instead.

What “A Wealth of Common Sense” Can Teach Us

The core of the “A Wealth of Common Sense” approach is this: focus less on perfect timing and more on sound decisions you can live with over time.

Instead of asking, “When will housing prices fall enough for me to get a deal?” a better question is, “What housing choice makes sense for my finances, my family, and my time horizon, given the market I live in today?”

Long-term data shows that U.S. home prices have generally trended upward, with occasional painful setbacks. That means waiting for a crash can backfire: you may avoid short-term risk but miss years of building equity or securing stable housing costs.

On the flip side, buying “just in case prices keep going up” is also a mistake if the monthly payment is unsustainable or your life situation is unstable. Common sense lives in the middle ground: buy when you’re financially ready, your job and life plans are reasonably stable, and you can commit to holding the property for at least 5–7 years.

Practical Moves for Buyers, Sellers, and Homeowners

For buyers

- Focus on the payment, not just the price. A slightly higher price at a lower rate may be cheaper monthly than a lower price at a higher rate.

- Run worst-case scenarios. Could you handle a job change, a surprise expense, or a slower-than-expected raise?

- Consider “good enough” instead of “forever home.” In an expensive market, a starter home or townhouse may be a smarter first step than waiting for your dream house.

For sellers

- Price for the market you’re actually in. Buyers today are extremely payment-sensitive. Overpricing leads to long listing times and bigger cuts later.

- Be ready to negotiate on concessions. Help with closing costs or rate buydowns can matter more than a small price change.

For current homeowners

- Protect your financial cushion. Even if your home value wobbles, a solid emergency fund keeps you in control.

- Think carefully about tapping equity. A home equity line can be useful, but turning your house into an ATM is how many people got hurt in the last crash.

Real-World Experiences with Waiting for Prices to Fall

Numbers and charts are useful, but a lot of the anxiety about housing comes from lived experience. Here are a few common storylines you’ll hear if you talk to enough buyers, sellers, and homeowners.

The couple who waited for “the crash” that never came (yet)

Imagine a couple renting in 2018. They see prices rising and think, “This is crazy; it has to come down.” They wait. In 2019, prices rise again they wait some more. Then 2020 hits, rates drop, and bidding wars start. They decide they definitely won’t buy in a frenzy. By 2021, the homes they once considered expensive now look like a bargain compared with new listings in their area.

Fast-forward to 2025. Prices have cooled off. Growth has slowed, and some markets are slightly down. But in their city, the starter home they wanted years ago still costs more than it did then, and mortgage rates are much higher. They didn’t lose everything by waiting they saved money and stayed flexible but the “huge crash” they were counting on never appeared in a way that made buying dramatically easier.

The buyer who “overpaid” and is still glad they bought

Now picture a first-time buyer who bought in 2022, right before rates surged. Friends told them they were crazy to pay that much. They worried the value might drop.

In the years that followed, prices in their metro barely moved, maybe up a little, maybe flat. On paper, they didn’t hit a home run. But their monthly payment stayed fixed. Rents around them kept rising. They painted the walls whatever color they wanted, adopted a dog, and turned a spare bedroom into a home office. Financially, they may not have timed the market perfectly. But for their lifestyle and long-term stability, the decision still feels right.

The seller who misread the market

On the other side, there’s the homeowner who listed in late 2023 assuming the pandemic boom rules still applied. They priced their home as if buyers would line up and waive inspections. Instead, showings were sparse, and the offers that did come in were cautious and full of contingencies.

After a few months on the market and several price cuts, they finally sold for slightly less than they could have gotten if they’d priced realistically from day one. Their story is a reminder that housing transitions slowly. The “peak” prices you read about on social media may be from a very different phase of the cycle than the one you’re actually selling into.

The common thread

These stories aren’t about heroes and villains. They’re about how hard it is to time a complex, slow-moving market. Most people don’t look back and say, “I nailed the exact bottom.” Instead, they say things like, “We bought when it made sense for us,” or, “We wish we’d moved a little sooner, but it still worked out.”

If there’s a “wealth of common sense” in housing, it’s this: you probably won’t buy or sell at the perfect moment. But you can still make a decision that works well for your life by grounding your choices in data, not fear and by accepting that housing is, first and foremost, a place to live, and only secondarily a spreadsheet of returns.