Table of Contents >> Show >> Hide

- Why Bull Markets Make Assessors Look Unbeatable

- How Property Assessment Really Works

- Why Your Value Can Rise Even If You Did “Absolutely Nothing”

- Why the Assessor Has Structural Advantages

- The Bull Market Tax Trap

- When the Assessor Does Not Fully Win

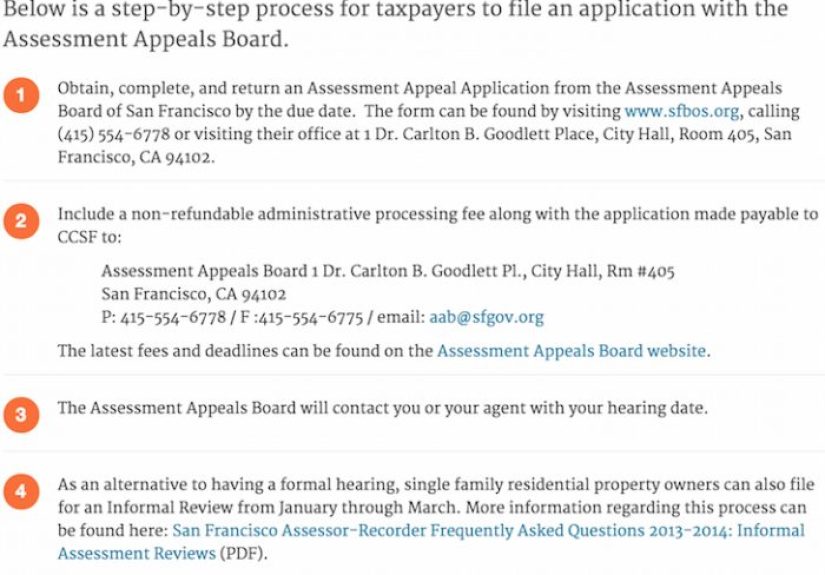

- How to Appeal Without Wasting Everyone’s Time

- Examples of How the Assessor “Wins” in Real Life

- What Smart Homeowners Do During a Bull Market

- The Bigger Lesson Behind the Title

- Experiences Homeowners Commonly Have in a Bull Market

- Conclusion

- SEO Tags

There are two kinds of homeowners in a booming real estate market. The first kind checks home-value websites every other weekend and whispers, “Look at us, building wealth.” The second kind opens the annual assessment notice and says something unprintable before making coffee strong enough to stand up on its own. Both people may be living in the same house.

That strange emotional whiplash is the heart of this topic. In a bull market, rising home prices feel fantastic when you are bragging at a barbecue, talking to your lender, or imagining your future net worth. But the same appreciation often turns into a higher assessed value, a fatter tax bill, and a frustrating lesson in how local government keeps score. That is why the phrase “the property assessor always wins in a bull market” feels painfully true.

Still, the title needs a little courtroom-style honesty. The assessor does not literally win every time. Homeowners can appeal. Some states cap assessment growth. Exemptions, tax limitations, and timing rules can slow the pain. But in an environment where comparable sales keep climbing, inventory stays tight, and buyers behave like they are chasing the last life raft on the Titanic, the system naturally pushes assessments upward. The wind is usually at the assessor’s back.

This article explains why that happens, how property assessments work, why bull markets create such a powerful tax machine, and what homeowners can actually do when their assessed value starts sprinting faster than their comfort level.

Why Bull Markets Make Assessors Look Unbeatable

A bull market in housing is simple in theory and expensive in practice. Prices rise across neighborhoods because demand is strong, supply is limited, incomes or credit conditions support higher bids, and buyers keep proving that yesterday’s “crazy price” is today’s starting point. Once that pattern shows up across enough sales, it becomes evidence. And assessors love evidence.

Most property assessment systems are built around market value, assessed value, or a formula tied to one or both. That means the assessor is not supposed to ask whether you personally enjoyed the appreciation. They are asking what the market seems to say your property would sell for under normal conditions. If similar homes nearby sold for more, your house may now look more valuable on paper even if you have not changed a single doorknob.

That is the first reason the assessor seems to “always win.” In a rising market, the data is usually pointing in one direction. Sales ratios, neighborhood trends, replacement cost models, and mass appraisal systems begin leaning upward together. Homeowners may feel singled out, but the assessor’s office is often just following the market’s breadcrumb trail straight to your mailbox.

How Property Assessment Really Works

Many homeowners confuse three different things: market value, assessed value, and tax bill. They sound like cousins, but they do not behave the same way.

Market Value

This is the estimated amount your property would likely sell for in an open and competitive market. Think of it as the “what would a typical buyer pay?” number. In many jurisdictions, the assessor tries to estimate this value using recent sales of comparable properties, cost approaches, or income approaches for investment properties.

Assessed Value

This is the taxable value assigned to your property. Sometimes it matches market value. Sometimes it is a fraction of market value. Sometimes it is limited by state rules, homestead caps, or reassessment laws. This is where things get spicy. Two homes with similar market values can face very different assessments depending on local law, exemption status, and ownership history.

Tax Bill

This is the result of assessed value multiplied by the relevant tax rate, adjusted for exemptions, credits, levies, and whatever other pieces your local tax system uses to keep accountants employed. If your taxes rise, it may be because your value rose, because the tax rate changed, or both. That distinction matters. Plenty of homeowners yell at the assessor when the real villain is the millage rate.

In other words, appreciation does not automatically translate dollar-for-dollar into taxes. But in a bull market, appreciation often sets the stage for the next round of tax pain.

Why Your Value Can Rise Even If You Did “Absolutely Nothing”

This is the classic homeowner complaint, and honestly, it is fair. If you did not add a pool, finish the basement, build a guest house, or install a kitchen fit for a cooking show, why should your assessment jump?

Because assessors are not only valuing your improvements. They are valuing your position in the market. Your home is part of a broader sales ecosystem. If buyers suddenly start paying more for houses on your street because the school district got hotter, remote work made your suburb trendy, or the city installed a new rail stop nearby, the market value of your property may rise even if your house stayed physically identical.

That feels unfair because homeowners tend to think in terms of effort: “I did not upgrade anything.” Assessors think in terms of evidence: “Comparable properties sold higher.” These two worldviews collide every year, and in a bull market the assessor’s version usually has the paperwork.

Why the Assessor Has Structural Advantages

Here is the uncomfortable truth: the property tax system is not a casual debate between equal parties. The assessor’s office begins with several built-in advantages.

1. The Assessor Has Better Data at Scale

Assessors work with large pools of sales data, parcel records, sketches, classifications, valuation models, and neighborhood trend reports. A homeowner may know their own kitchen better than anyone on Earth, but the assessor knows how hundreds of nearby properties are behaving in the aggregate.

2. The System Presumes a Process

Appeal procedures exist, but they are structured. Deadlines are short. Forms are specific. Evidence rules matter. Homeowners who show up with righteous anger and three screenshots from a home-search app often discover that emotion is not an accepted appraisal methodology.

3. Bull Markets Produce Friendly Comparables

In a soft market, homeowners can argue that sales are weak, listings are stale, and buyers are scarce. In a bull market, the comps often look muscular. If several homes like yours sold high, the assessor walks into the room with backup singers.

4. Most Owners Appeal Late or Poorly

Homeowners often wait until the tax bill arrives, not realizing the fight should have started earlier at the valuation stage. Others appeal the taxes instead of the assessment, or they bring evidence that is irrelevant, outdated, or emotionally satisfying but legally useless.

The Bull Market Tax Trap

The reason this topic matters is not just that assessments rise. It is that bull markets create a tax trap that catches homeowners in stages.

Stage one is psychological: you feel richer. Stage two is administrative: the assessor updates value. Stage three is financial: your escrow payment rises, your monthly housing cost jumps, and you realize that “paper wealth” has a side hustle as a recurring expense.

This trap is especially brutal for longtime owners on fixed incomes. Their house may be worth dramatically more than it was a decade ago, but that does not mean their cash flow improved. A retiree can become asset-rich and budget-poor at the exact same time. That is where exemptions, freeze programs, circuit breakers, assessment caps, and homestead protections become more than policy jargon. They become survival tools.

When the Assessor Does Not Fully Win

Now for the good news. The assessor’s office may have momentum, but homeowners are not powerless decorative shrubs. There are several situations where you can push back effectively.

Your Property Record Is Wrong

If the assessor thinks you have 2,800 square feet but you have 2,350, that is not a philosophical disagreement. That is a fixable error. The same applies if the record shows a finished basement, extra bathroom, superior condition, or additional improvements that do not exist.

Your Comparable Sales Are Better Than Theirs

The best appeal evidence is usually a set of recent, relevant comparable sales that reflect your property’s actual condition, size, location, and features. If the assessor used shiny, renovated sales while your home still has countertops from the Bush administration, you may have a case.

Your House Has Real Negative Features

Busy roads, awkward layouts, deferred maintenance, drainage issues, outdated systems, neighborhood nuisances, or functional obsolescence can all matter. Buyers discount these things. Assessors should too.

Your State Has Caps, Limits, or Exemptions

In many states, the market may rise faster than your taxable value because local law limits assessment growth or offers homestead protections. These rules do not erase taxes, but they can slow the climb. That is one reason neighbors with similar homes can face dramatically different bills.

How to Appeal Without Wasting Everyone’s Time

If you are going to challenge an assessment, do it like a grown-up with receipts.

Start With the Assessment Notice, Not the Tax Bill

Check deadlines immediately. Many owners wait too long and end up trying to argue with a system that has already moved to the next season. Once deadlines pass, your options narrow fast.

Review the Property Card

Confirm the basics: square footage, lot size, construction quality, room count, condition, age, finished areas, and any special features. Small mistakes can create large valuation errors.

Use Better Comparable Sales

Look for recent sales of similar homes in your neighborhood or competing area. Avoid dream comps from across town. Avoid active listings unless your jurisdiction allows them as supporting evidence. Closed sales are usually stronger.

Document Condition Honestly

Photos matter. So do repair estimates, contractor opinions, inspection reports, and records of issues that reduce value. The key word is “reduce.” The assessor does not care that you dislike beige paint. They care whether the market would discount the home.

Be Calm and Specific

Do not tell the board that taxes are too high “because everything is ridiculous now.” They probably agree, but that is not the question. The question is whether your assessed value is accurate under the law.

Examples of How the Assessor “Wins” in Real Life

Example 1: The Fast-Rising Suburb. A homeowner bought in 2019 for $350,000. By 2025, similar homes nearby sold between $490,000 and $530,000. The owner has done almost nothing to the property except replace a dishwasher and complain creatively. The assessor raises market value significantly. The owner feels blindsided, but the surrounding sales make the increase hard to defeat.

Example 2: The Gentrifying City Block. A modest older home sits near a corridor that suddenly attracts restaurants, transit investment, and renovation activity. Buyers start paying up for location. Even if the house itself remains rough around the edges, land value and neighborhood desirability pull the assessment upward.

Example 3: The Capped Homestead vs. New Buyer. One owner has lived in a home for years under a capped assessment system. A similar property next door sells at a much higher price and resets closer to market. Same street, similar houses, very different tax stories. In bull markets, timing can matter almost as much as property condition.

What Smart Homeowners Do During a Bull Market

Homeowners who handle bull markets well do not treat assessment notices as junk mail. They read them early, keep records, understand local exemptions, and budget for the possibility that rising equity may come with rising carrying costs.

They also stop assuming that online home-value estimates are useful only when the number is flattering. If you love the Zestimate at dinner parties but hate the assessment notice in private, congratulations: you have discovered selective valuation morality.

More seriously, smart owners understand that a hot market has two financial consequences. It may improve net worth, but it can also affect taxes, insurance, maintenance expectations, and resale calculations. Appreciation is not just a trophy. It is a cost event.

The Bigger Lesson Behind the Title

“The property assessor always wins in a bull market” is really shorthand for a broader truth: public valuation systems are designed to absorb market signals, and booming markets send loud signals. When the sales data is strong, the burden shifts to the homeowner to prove that their specific property deserves different treatment.

That does not mean the system is evil. It means the system is mechanical. Local governments rely on property taxes to fund schools, infrastructure, emergency services, and daily operations. When property markets move, the tax base eventually moves too. The friction comes from the fact that your paycheck does not always appreciate as quickly as your neighborhood.

So yes, in a bull market, the assessor often looks unbeatable. But the real winner is not the assessor personally. It is the combination of rising comparable sales, statutory valuation rules, limited homeowner preparation, and the government’s need for a stable tax base. The assessor is simply the face on the envelope.

Experiences Homeowners Commonly Have in a Bull Market

Ask enough homeowners about assessments during a bull market and the stories start sounding like a national support group with better landscaping. One owner says the first clue was not the assessment notice but the escrow analysis from the mortgage servicer. Another says the warning sign was when three nearly identical homes on the block sold in a single month for prices that made everyone gasp and immediately check their own equity. A third says the real shock came when they realized being “house rich” did not help them pay a bigger monthly bill.

A common experience is the emotional contradiction. People feel proud that their home is worth more and annoyed that the tax system noticed. They want the market value when refinancing, borrowing, bragging, or planning a sale. They want a different value entirely when the county gets involved. It is human nature, and it is also why assessment season feels like a neighborhood-wide identity crisis.

Another common experience is confusion. Homeowners receive a notice with unfamiliar terms, percentages, deadlines, and a value that seems to have appeared out of thin air. They assume someone inspected every room with a magnifying glass. Often, the reality is more mundane: mass appraisal models, recent comparable sales, and existing property records did the heavy lifting. That gap between how personal the bill feels and how statistical the process really is can be maddening.

Then there is the appeal experience. Some owners walk in prepared and do well. They bring photos showing deferred maintenance, accurate square footage, and better comps than the assessor used. Others learn the hard way that “my taxes are too high” is not an argument. Boards want evidence, not vibes. The most successful homeowners usually approach appeals like a case file, not a venting session.

Longtime owners often describe a deeper frustration. They are not speculators. They are not flipping houses. They are just living in the same home while the market around them catches fire. When values rise quickly, they may feel punished for staying put. Their neighborhood becomes more desirable, but their monthly costs rise with it. For retirees, widows, or families on tight budgets, the assessment notice can feel less like validation and more like a warning shot.

Newer buyers, meanwhile, have a different story. They often buy at a high market price and then act surprised when the assessment catches up. In states where a sale triggers a reassessment or resets taxable value, that first post-purchase notice can be a brutal education. The previous owner’s lower tax bill suddenly looks like ancient folklore.

And yet, there is also a practical side to these experiences. Many homeowners who go through one rough assessment cycle become much smarter afterward. They learn deadlines. They learn what homestead protections exist. They learn to check their property card, save records, and treat local tax policy as part of homeownership rather than as random punishment from the sky. In that sense, the bull market creates better-informed owners, even while it empties their wallets a little faster.

Maybe that is the final real-world lesson. The assessor seems to win in a bull market because the market is doing most of the work. But homeowners who understand the rules, organize their evidence, and pay attention early can still avoid the worst surprises. You may not beat the trend, but you can absolutely stop donating points to it.

Conclusion

In a rising housing market, the property assessor often feels unbeatable because the system rewards market evidence, and bull markets generate plenty of it. As comparable sales climb, assessments tend to follow, even for owners who have not remodeled, expanded, or changed much at all. That can turn home appreciation into a higher recurring cost at exactly the moment owners thought they were “winning.”

But the headline is only half the story. Homeowners still have leverage when records are wrong, comps are weak, condition issues are ignored, or local exemptions and caps are underused. The real advantage goes to people who understand how assessments work before the tax bill lands. In other words, the assessor may have momentum in a bull market, but preparation is still the homeowner’s best counterpunch.