Table of Contents >> Show >> Hide

- Why VC Failure Doesn’t Look Like Normal Failure

- The Real Risk: Under-Owning the Home Run

- How Funds Accidentally Optimize for Looking Smart Instead of Being Right

- Reserves, Pro Rata, and the Boring Mechanics That Decide Whether a Fund Wins

- Why This Risk Gets Worse in Tough Markets

- What Strong Venture Firms Do Differently

- What Founders Should Learn From This

- The Bottom Line

- Experiences From the Real World of the Other Failure Risk in VC

Everyone knows the obvious failure risk in venture capital: backing a company that flames out, runs out of cash, and leaves behind a pitch deck, a Slack graveyard, and one very lonely standing desk. That risk is real. Startups fail all the time. Founders misread markets, teams break, products drift, timing betrays them, and sometimes the “revolutionary platform” is just a nicer way to send invoices.

But that is not the only failure risk in VC. In many cases, it is not even the scariest one.

The other failure risk is missing the outlier. Or worse: finding it, backing it, and still not owning enough of it when the dust settles.

That is the quiet terror hiding underneath venture math. A fund can survive a bunch of dead startups. It is built for that. What it may not survive is a portfolio full of decent decisions that never compound into a truly exceptional outcome. In venture capital, losing money on the obvious losers is painful. Missing the one weird, explosive winner that could return the fund is existential.

This is what makes venture such a strange business. In most fields, avoiding mistakes is a pretty good strategy. In VC, avoiding mistakes can turn into its own mistake. A firm can be disciplined, rational, cautious, and respectable all the way to mediocrity. That is not because discipline is bad. It is because venture capital is not a game of averages. It is a game of asymmetry.

Why VC Failure Doesn’t Look Like Normal Failure

In a normal business, you try to minimize downside and stack up a reliable series of wins. In venture, that logic only gets you halfway there. A portfolio can contain plenty of “fine” companies, some modest exits, a few acqui-hires, maybe even a respectable merger or two, and still fail to produce a great fund.

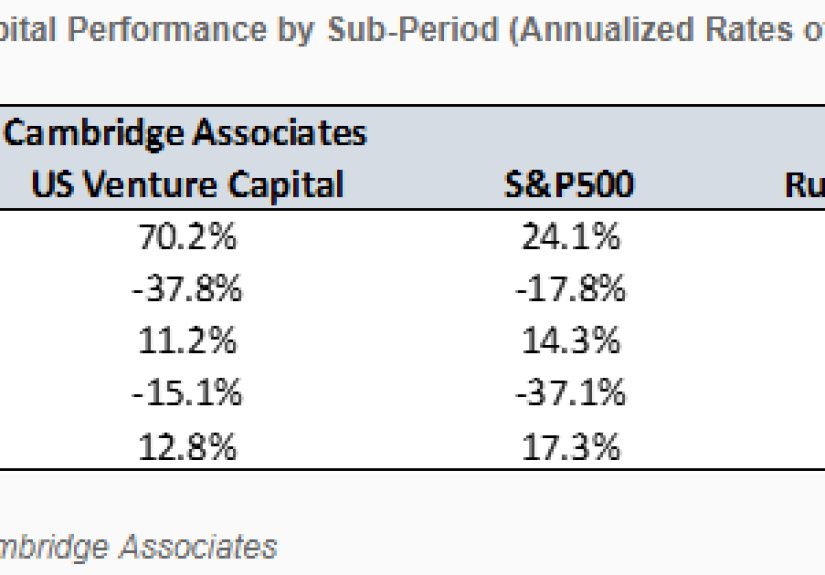

That sounds ridiculous until you remember how power law returns work. Venture outcomes do not line up neatly around the middle. They clump at the bottom and explode at the top. A tiny number of companies create a wildly disproportionate share of value. That means the math of fund performance often depends less on avoiding the bad companies than on making sure you actually capture enough of the rare great ones.

In other words, venture is not just about picking winners. It is about picking enough of the right winners, with enough conviction, with enough follow-on capacity, and with enough ownership discipline that the win still matters after dilution, time, and market chaos have had their turn with the cap table.

This is where many funds stumble. They tell themselves the story that they failed because some startups went to zero. Sometimes that is true. But often the deeper problem is this: they built a portfolio that was too timid, too thinly spread, too diluted, or too reluctant to press advantage when the signal finally arrived.

The Real Risk: Under-Owning the Home Run

Let’s say a seed fund invests in 30 companies. That sounds diversified. Sensible. Mature, even. The website will look fantastic. Lots of logos. Lots of smiling founders. Plenty of “category-defining” language floating in the air like expensive cologne.

Then one company starts to separate. Revenue is compounding. Customers actually love the product. Hiring gets easier instead of harder. The founder somehow gets calmer when things get more chaotic, which is usually a good sign and occasionally proof they are a wizard.

Now the real test begins.

Does the fund have reserves to keep investing? Does it have pro rata rights? Will the partners actually use them? Will they lean in when the company looks expensive, or will they get spooked by valuation and save their cash for “more balanced opportunities,” which is venture-speak for “we are about to make a very cautious mistake”?

Plenty of firms discover their biggest risk too late. They got into the company early, but not heavily enough. They reserved too little capital. They spread the fund across too many bets. They treated follow-on investing as optional rather than strategic. By the time the breakout became obvious, the price of conviction had gone up. Then dilution did what dilution does: it smiled politely and stole the upside.

This is the other failure risk in VC. It is not merely failing to identify greatness. It is failing to structurally benefit from it.

How Funds Accidentally Optimize for Looking Smart Instead of Being Right

One of the most common traps in venture is building a decision process around social safety instead of portfolio outcomes.

A partner who backs a weird company that fails can look reckless. A partner who passes on a weird company that later becomes enormous can still look reasonable for a while, especially if everyone else passed too. That is the danger. Career risk and fund risk are cousins, not twins. A firm can quietly train itself to avoid embarrassment rather than maximize returns.

This creates a subtle but powerful bias toward consensus. Consensus is comfortable. Consensus also tends to be expensive and late. By the time everyone agrees a company is excellent, the round is crowded, the valuation is richer, and the cheapest ownership is a memory.

The firms that outperform usually do something emotionally difficult: they take idiosyncratic risk early, then increase exposure when the data starts confirming the original thesis. They do not just want a front-row seat at the show. They want enough ownership that the applause turns into returns.

That sounds obvious. It is not. Many investors are far more comfortable making the first check than the second or third. Initial checks feel exploratory. Follow-ons feel like judgment. And judgment, unfortunately, can be observed by other adults.

Reserves, Pro Rata, and the Boring Mechanics That Decide Whether a Fund Wins

Venture loves mythology. Founder intuition. lightning in a bottle. pattern recognition. These things matter. But some of the biggest differences in fund outcomes come from mechanics that are far less cinematic.

Reserve strategy is one of them.

If a fund does not intentionally set aside capital for follow-on investments, it may be forced into a terrible choice later: support emerging winners or keep making new deals to maintain pipeline optics. That is like bringing a water gun to a forest fire and calling it capital allocation.

Reserves matter because early ownership rarely stays still. As startups raise additional rounds, everyone gets diluted unless they continue participating. That means a fund’s apparent early exposure can shrink dramatically by exit. A promising 10% ownership stake can become something much smaller over time. If the company becomes huge, that difference is not cosmetic. It can be the difference between “great investment” and “great company that did not move the fund.”

Pro rata rights also matter, but having them is not the same as using them well. Some investors cling to pro rata mechanically, topping up across the board without enough discrimination. Others underuse it because they become too valuation-sensitive in the very companies most likely to grow into those valuations. The best firms do neither. They treat follow-on decisions as a portfolio construction question, not just a company-by-company question.

That means asking hard questions. If I put the next dollar into this company, what is the expected upside from here? How much dilution am I preventing? What ownership do I need at exit for this outcome to matter? What am I giving up elsewhere in the fund by making this choice now?

Those are not glamorous questions. They are also the questions that keep a good company from becoming a wasted win.

Why This Risk Gets Worse in Tough Markets

When the market gets choppy, the other failure risk becomes even more dangerous.

In tighter fundraising environments, investors often concentrate capital into fewer portfolio companies. That can be smart. It can also expose poor planning. A fund that looked diversified in a hot market may realize too late that it lacks the reserves to defend ownership in its strongest businesses. Suddenly every follow-on becomes triage.

At the same time, headline valuations can distort judgment. On paper, a company may look extraordinary. In reality, later financings often come with preferences, protections, and terms that make common equity less valuable than the headline number suggests. That matters to founders, employees, and earlier investors alike. If a fund manager is dazzled by the top-line valuation and ignores the structure underneath, they may misjudge both risk and return.

So the challenge is not simply “invest more in winners.” The challenge is “invest more in winners with sober assumptions about dilution, exit structure, and future financing.” That is harder, less tweetable, and much more useful.

What Strong Venture Firms Do Differently

The best venture firms take the other failure risk seriously long before it shows up in quarterly reporting.

1. They build the fund around ownership, not just access.

Getting into a round is nice. Owning enough for the outcome to matter is nicer. Great firms think about check size, target ownership, dilution paths, and reserve needs from day one.

2. They separate company quality from fund impact.

A company can be good and still not be meaningful for a given fund. That sounds harsh, but it is simply math. Strong investors know the difference between “I like this business” and “this outcome can return a serious portion of the fund.”

3. They use follow-on investing as strategy, not sentiment.

They do not double down out of loyalty or fear of signaling. They do it because the expected return on the next dollar is compelling relative to the rest of the portfolio.

4. They leave room for conviction.

Some funds are so overdiversified that they have no ability to express conviction later. That may reduce regret, but it also reduces the chance of exceptional performance.

5. They are honest with LPs about how venture really works.

Great funds do not pretend every company is on track. They explain that venture returns are concentrated, reserves are precious, and capital must be concentrated when the evidence justifies it.

What Founders Should Learn From This

This lesson is not just for investors. Founders should pay attention too.

Not all capital is equally helpful once a company starts working. An investor who can write the first check but cannot support later rounds may still be valuable, but founders should understand the trade-offs. If a fund lacks reserves, lacks conviction, or has a history of going quiet at the first sign of a tough quarter, that matters.

Founders often assume the biggest risk is hearing “no.” Sometimes the bigger risk is hearing “yes” from an investor whose strategy is misaligned with the company’s likely path. If your business needs patient backing, follow-on support, and long-term ownership partnership, a fast, flashy, low-conviction investor can create more problems than a clean pass ever would.

So when founders evaluate VCs, they should ask a few uncomfortable questions. How does this fund think about reserves? How often do they follow on? What ownership do they target? When they believe, do they really believe, or do they just post encouraging comments on LinkedIn and disappear when the board deck gets spicy?

The Bottom Line

The headline risk in venture capital is startup failure. The deeper risk is portfolio irrelevance.

A fund can survive strikeouts. It is designed to. What it cannot easily survive is a strategy that repeatedly under-owns the breakout, under-reserves for the obvious winner, or confuses caution with intelligence. Venture capital is full of stories about companies that died. It should spend more time talking about the great companies that were seen, touched, and still not captured in a meaningful way.

That is the other failure risk in VC: not losing on the losers, but failing to win big enough on the winners.

And in this business, that is often the mistake that matters most.

Experiences From the Real World of the Other Failure Risk in VC

Talk to people who have spent time around venture, and you hear a pattern that is less dramatic than a startup implosion but often more painful in hindsight. It usually starts with a company that did not look obvious enough at the beginning. Maybe the market seemed too small. Maybe the founder was unusual. Maybe the product looked weird before it looked inevitable, which is honestly how many great products introduce themselves.

At first, the investment gets approved almost reluctantly. A small check goes in. The firm tells itself it is “getting exposure,” which sounds smart until you realize exposure is not the same thing as ownership. Months later, the company starts to work. Customers stick. Revenue quality improves. The founder keeps shipping. Talent shows up without needing to be bribed with a company retreat in Napa and twelve varieties of sparkling water.

This is the moment when experience matters. The strongest investors get more serious as the evidence improves. The weaker ones get nervous. They worry the valuation has run too far. They worry about concentration. They worry the next round will make them look foolish if the company stalls. So they hesitate. They trim. They “stay disciplined” in the narrowest possible sense.

Then the company keeps winning.

Years later, the firm still puts the logo on its website. It still mentions the deal in fundraising conversations. But internally, people know the truth: the ownership stake got too small, too early, and the fund did not benefit the way it should have. The company became famous. The investment became a case study. The actual return became, at best, nice. In venture, “nice” is a dangerous word.

There is another version of this experience too. A firm reserves plenty of capital, but it spreads conviction too evenly. Instead of leaning hardest into the strongest signals, it treats follow-ons as a fairness exercise across the portfolio. Everyone gets a little support. Nobody gets enough. This feels balanced. It also tends to flatten upside. Venture is not a participation trophy business. The portfolio does not care whether your internal process felt emotionally equitable.

Founders feel this dynamic from the other side. Many can tell which investors are truly built for the long haul and which ones mainly enjoy the courtship phase. The best investors get sharper as the company grows. The weaker ones become ceremonial. They attend the meeting, nod at the metrics, ask one question about burn, and then vanish like a magician who only knows one trick.

That is why the other failure risk in VC is so instructive. It reveals that venture success is not just about taste. It is about structure, patience, and courage. You need taste to get in early. You need structure to preserve ownership. You need patience to hold through messy middle chapters. And you need courage to keep backing the rare company that is actually bending the curve. Plenty of firms can do one or two of those things. Very few do all four consistently. Those are usually the firms everyone else studies later and pretends were obvious all along.