Table of Contents >> Show >> Hide

- First, what an “all-time high” actually means

- The “everything bagel” of all-time highs

- Stocks at all-time highs: not a warning label, more like a feature

- Gold and Bitcoin at highs: “contradiction” is not a law of physics

- Housing at highs (even with high mortgage rates): the supply story matters

- GDP and household net worth: why these records are common (and still meaningful)

- Why all-time highs make smart people do dumb things

- Hindsight bias: the sneakiest “I knew it” in the world

- A practical playbook for investing when “everything” is at a high

- Bottom line: record highs are not a signal to freeze

- Experiences: What “New All-Time Highs in Everything” Feels Like in Real Life (and How People Get Through It)

- SEO Tags

If you’ve felt like the world is screaming, “NEW ALL-TIME HIGH!” at you every time you open your phonecongrats, your nervous system is working as designed.

Stocks? High. Housing? High. The economy? Bigger. Your neighbor’s confidence? Somehow also at an all-time high. It can feel like we’re living inside a

CNBC chyron… except the chyron is inside your brain.

Ben Carlson at A Wealth of Common Sense framed this perfectly: when “everything” is making new highs at once, it’s equal parts fascinating and

disorienting. And the disorientation is the important partbecause it’s usually what triggers bad financial decisions disguised as “being cautious.”

Let’s unpack what all-time highs really mean, why they’re more normal than they feel, and how to handle them like an adult (the kind of adult who has a

spreadsheet, not the kind who impulse-buys a doomsday dehydrator).

First, what an “all-time high” actually means

An all-time high is simply the highest level something has ever reached in the dataset you’re looking at. That sounds obvious, but it matters.

“All-time highs” are often quoted in nominal terms (not adjusted for inflation). Nominal numbers tend to set records over time because

economies grow, populations increase, companies innovate, and yesprices rise.

That doesn’t make the highs “fake.” It just means you should ask a better follow-up question:

Is this a nominal high, a real (inflation-adjusted) high, or a “feels-high-because-the-news-is-loud” high?

In other words: sometimes the chart is screaming. Sometimes the chart is whispering. And sometimes the chart is normal, but the internet is yelling.

The “everything bagel” of all-time highs

When people say “everything is at an all-time high,” they’re usually pointing to a mix of assets and economic indicators that don’t normally party in the

same corner of the room:

- U.S. stocks (major indexes pushing to new peaks)

- Gold (often viewed as a hedge or “safety” asset)

- Bitcoin/crypto (a risk-on roller coaster with a fan club)

- Housing prices (home values and price indexes climbing)

- GDP (the economy’s “size” in dollars)

- Household net worth (the combined balance sheet of households)

- And sometimes… sports teams (because life has a sense of humor)

The point isn’t that every one of these is “overvalued.” The point is that when many of them are high at once, it can make investors feel like they missed

the boatand the brain responds to that feeling by trying to regain control.

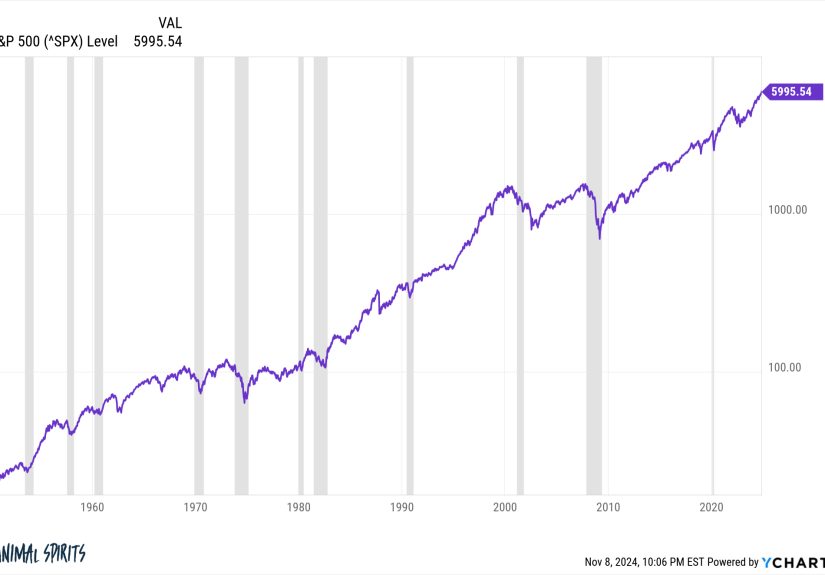

Stocks at all-time highs: not a warning label, more like a feature

Here’s the part that shocks people the first time they hear it: healthy markets spend a lot of time near highs. If markets went up in a straight line,

investing would be easy… and also completely terrifying for other reasons.

Why new highs happen

Over long periods, stock indexes rise because the underlying businesses grow: revenues expand, earnings increase, dividends get paid, and productivity

improves. That doesn’t mean every year is good. It means the long-term trend is up often enough that “record highs” show up regularly in the data.

Vanguard, Fidelity, Schwab, and Morningstar all make the same practical point in different words:

all-time highs are usually a sign of strength, and trying to time around them can backfire.

A quick reality check: an index is not “the economy”

The S&P 500 is a widely used gauge of large U.S. companies, not a complete picture of the entire economy and definitely not a guarantee of future

returns. It’s also worth remembering that many widely shared charts show a price index, not a total-return index (which would include dividends).

That nuance matters when people compare “levels” across decades.

Gold and Bitcoin at highs: “contradiction” is not a law of physics

People love telling a simple story: “If stocks are up, gold should be down,” or “If gold is up, crypto should be down,” or “If everyone is happy, something

bad must happen by Friday.” Markets do not sign these agreements.

Gold can rise for reasons like inflation concerns, geopolitical uncertainty, central bank demand, or a desire for diversification. Bitcoin can rise because

of liquidity, investor risk appetite, narratives about adoption, or the simple reality that it trades like a caffeinated tech stock sometimes.

Both can go up at the same time if different groups are buying for different reasonsor if the common driver is “money is sloshing around and humans are

emotional.” That last one is surprisingly common.

Housing at highs (even with high mortgage rates): the supply story matters

Housing is where people get the most confused, because it feels personal. A stock chart is a line. A home price is your future, your commute, and whether

your kitchen has enough counter space for emotional support snacks.

Home prices can push to new highs even when mortgage rates are elevated because housing is shaped by slow-moving constraints:

limited supply in many areas, homeowners who don’t want to sell and give up their existing low-rate mortgages, demographics, local job markets, and the

fact that “building more homes” is harder than tweeting “just build more homes.”

The big takeaway: housing is not a single national market. It’s thousands of local markets wearing a trench coat.

GDP and household net worth: why these records are common (and still meaningful)

Nominal GDP tends to reach new highs over time because it reflects the dollar value of what the economy produces. If the economy grows and prices rise,

nominal GDP usually follows. That’s not a reason to celebrate or panic by itself; it’s a reminder to interpret “record high” in context.

Household net worth can also hit records when asset prices rise (stocks and home values) and when savings or business values increase. In plain English:

if the things households own go up, the household balance sheet goes up too.

But here’s the crucial nuance: “total household net worth” is an aggregate number. It can rise while many households still feel squeezed. That gap between

the macro chart and the lived experience is one reason narratives swing so violentlypeople aren’t imagining the stress; they’re just not reading the same

spreadsheet.

Why all-time highs make smart people do dumb things

All-time highs trigger a specific mental cocktail:

- Anchoring: “If I buy now and it drops, I’ll feel stupid.”

- Loss aversion: Losses hurt more than gains feel good, so “doing nothing” feels safer.

- Recency bias: Whatever just happened feels like what will keep happening.

- FOMO: “Everyone’s getting rich without me,” which is never trueand always emotionally persuasive.

- Control-seeking: When uncertainty rises, the brain wants a lever to pull.

That’s how you end up with investors who have a long-term plan but a short-term emotional Wi-Fi connection. One scary headline later, the plan disappears

and gets replaced with a vibe.

Hindsight bias: the sneakiest “I knew it” in the world

Carlson joked that we may be at all-time highs for hindsight bias toobecause once outcomes are known, narratives tighten up fast. Suddenly, the result was

“obvious.” Suddenly, everyone “called it.” Suddenly, you are surrounded by prophets who somehow forgot to place the trade.

Psychologists call this hindsight bias: after an event happens, we overestimate how predictable it was. This matters for investors because

it creates fake confidence. If you believe the past was obvious, you’ll believe the future is obvious tooand that’s when people start swinging for fences.

The antidote is humility with receipts: write down what you believe before outcomes occur, and review it later. Most “obvious” outcomes stop

looking so obvious when you replay the uncertainty in real time.

A practical playbook for investing when “everything” is at a high

You don’t need a heroic prediction. You need a process that survives your emotions.

1) Re-commit to your time horizon (and stop grading yourself daily)

If your goal is 10+ years away, daily market moves are mostly noise. That doesn’t mean “ignore risk.” It means align your attention with your timeline.

Watching a long-term plan on a 24-hour news cycle is like trying to raise a kid using only their report card from Monday.

2) Use dollar-cost averaging if fear is blocking action

If you have a lump sum but the idea of investing at a high makes you nauseous, dollar-cost averaging can be a behavioral bridge: invest a set amount on a

schedule. It’s not magic and it doesn’t guarantee better returns than investing all at once. But it can help you actually do the thing your plan

requires instead of waiting forever for “a better entry.”

3) Rebalance instead of trying to time the top

Rebalancing is the boring superhero of personal finance. When stocks run up, your portfolio can drift toward more risk than you intended. Rebalancing is

how you trim what’s grown and add to what’s laggedwithout pretending you know what the market will do next week.

4) Diversify with a reason, not a mood

“Everything is at an all-time high” can tempt people to overcorrectselling stocks to buy something that “hasn’t run yet,” or loading up on a single

“safe” asset. Diversification works best when it’s designed around your goals: growth, stability, income, inflation protection, and your ability to stay

invested when volatility shows up uninvited.

5) Watch concentration risk

When indexes hit highs, leadership can be narrow. If a handful of mega-cap stocks are doing most of the lifting, your portfolio may be more concentrated

than you realize, especially if you hold cap-weighted index funds plus extra “favorite” tech names on top. Concentration can juice returns on the way up

and magnify regret on the way down.

6) Set expectations that won’t betray you

The market does not pay you for being right in the short term. It (sometimes) rewards you for enduring uncertainty over time. That endurance includes:

pullbacks, boring stretches, headlines that feel like personal attacks, and the occasional moment where your portfolio looks like it tripped down the stairs.

If you expect “all-time highs” to be followed by a smooth ride, you’ll panic at the first pothole. If you expect volatility as a normal admission price,

you’ll be less shocked when it shows up.

Bottom line: record highs are not a signal to freeze

New all-time highs in everything can feel like the market is daring you to make a mistake. The best response usually isn’t dramatic. It’s disciplined:

stick to your plan, invest consistently, rebalance, diversify, and keep your emotional support decisions away from your financial accounts.

The irony is that long-term wealth often requires living through lots of “scary highs” and “scary drops” without letting either one bully you into bad timing.

If you can do that, you don’t need to predict the future. You just need to stay in the game.

Experiences: What “New All-Time Highs in Everything” Feels Like in Real Life (and How People Get Through It)

Even when you understand the logic, all-time highs can still feel weird in your bones. Investors don’t experience markets as math; they experience markets

as stories. And when the story is “everything is up,” the brain immediately writes a sequel called “therefore everything will crash.” That sequel

is not guaranteed, but it is extremely popular.

One common experience is the “I should have” spiral. Stocks hit new highs and you think, “I should have invested more.” Housing prices rise and you think,

“I should have bought earlier.” Bitcoin runs and you think, “I should have held.” Gold climbs and you think, “I should have diversified sooner.” Notice

how your brain never says, “I should have done exactly the right thing at exactly the right time while also sleeping eight hours and drinking enough water.”

The brain is not a wellness coach. It’s a highlight reel editor with a cruel streak.

Another experience is the “permission slip hunt.” When markets are high, people go searching for someoneanyoneto tell them it’s okay to invest. They read

ten articles, watch five videos, and ask three friends. If the friend who’s always bearish says “it’s too late,” they feel validated in doing nothing.

If the friend who’s always bullish says “this is just the start,” they feel validated in buying more. The goal becomes emotional relief, not better decisions.

Then there’s the awkward moment when your plan works and you don’t trust it. Your diversified portfolio is up, your automatic contributions keep firing,

and you start thinking, “This can’t be right.” That’s when some people sabotage themselves by chasing a more exciting narrativetrying to trade around highs,

jumping into concentrated bets, or rotating into whatever feels “undervalued” on a chart they found in a comment section.

The investors who handle all-time highs best often describe a different experience: they shrink the problem to what they can control. They stop treating

the market like a test they must pass and start treating it like weather. You don’t “win” by predicting rain; you win by owning an umbrella.

Practically, that looks like setting a contribution schedule and letting it run. It looks like checking allocations quarterly instead of doom-scrolling

daily. It looks like rebalancing when something gets too big, not because you’re calling a top, but because you’re respecting risk. It looks like keeping a

cash buffer so you don’t feel trapped. It looks like talking about your goals more than your returns.

And yes, it looks like occasionally muting finance apps and going outside to remember that your portfolio is a tool, not a scoreboard for your self-worth.

All-time highs are emotionally loud, but the best investing habits are quiet. The “experience” that builds wealth is rarely thrilling. It’s repeating a

sensible process so many times that it starts to feel boringwhich is exactly when it starts to work.