Table of Contents >> Show >> Hide

- Before the 10 Tips: Know What You’re Recording

- Tip 1: Decide Whether It’s a Contribution, an Exchange, or a Conditional “Not Yet”

- Tip 2: Recognize Donated Assets at Fair ValueThen Back It Up

- Tip 3: Use the Right Journal Entry Pattern (Asset + Revenue, Often with Matching Expense)

- Tip 4: Separate “Financial Assets” from “Nonfinancial Assets” in Your Reporting

- Tip 5: Treat Donated Securities Like InvestmentsBecause That’s What They Are

- Tip 6: Record Donated Fixed Assets (PPE) with a Plan for Depreciation and Restrictions

- Tip 7: Donated Inventory for Resale Needs a “Use vs. Sell” Decision Up Front

- Tip 8: Only Record Donated Services When They Meet Recognition Criteria

- Tip 9: Build a Repeatable Valuation Playbook (Not a “Valuation Mood Board”)

- Tip 10: Design Your Tracking for DisclosuresSo Year-End Isn’t a Treasure Hunt

- Common Recording Scenarios (Quick Examples)

- Real-World Experiences: What This Looks Like Outside a Textbook (About )

- Conclusion: Make Donated Assets Boring (In the Best Way)

Donated assets are the accounting world’s version of a surprise party: exciting, generous, andif you don’t plan aheadcapable of leaving glitter in places

you didn’t know existed (like your year-end close). Whether you’re a nonprofit receiving gifts-in-kind, a school logging donated supplies, or a small

organization that just got handed “a gently used printer” (translation: a 2009 spaceship with paper jams), recording donated assets correctly matters.

It impacts your financial statements, your compliance posture, your audit experience, and the story you tell funders about how resources are used.

This guide walks through practical, U.S.-based recording practices under common GAAP conceptsespecially the realities nonprofits face with in-kind gifts.

You’ll get 10 field-tested recording tips, specific examples (including sample journal entries), and a final “what it feels like in real life” section to

help you avoid the most common donated-asset faceplants.

Quick vocabulary check: “Donated assets” often means noncash gifts (equipment, inventory, stock, land, software, services). Many

organizations call these in-kind donations or contributed nonfinancial assets. The accounting goal is the same:

capture what you received, value it reasonably, classify it consistently, and document it so an auditor (or future you) can follow the breadcrumbs.

Before the 10 Tips: Know What You’re Recording

Donated assets usually fall into a few buckets

- Physical goods: supplies, food, clothing, medicine, books, furniture, computers.

- Long-lived assets (PPE): vehicles, equipment, buildings, land, leasehold improvements.

- Financial assets: publicly traded stock, mutual funds, bonds, sometimes crypto.

- Services: pro bono legal work, volunteer nursing, donated construction labor, design services.

You’ll record these differently depending on (1) what the item is, (2) whether you will use it or sell it, and (3) whether there are

any donor restrictions or conditions attached.

Friendly caution: This article is educational, not legal or tax advice. When donations get large, complex, restricted, or weird (hello, donated

livestock), involve a CPA who works with your type of organization.

Tip 1: Decide Whether It’s a Contribution, an Exchange, or a Conditional “Not Yet”

Not every “donation-ish” transaction is automatically contribution revenue. Start by asking: did the donor receive something of commensurate value

in return? If yes, you may be dealing with an exchange transaction. If no, it’s typically a contribution.

Next, watch for the “conditional contribution” trap: some gifts (especially grants) have a barrier to overcome and a right of

return/release if you don’t meet it. Those generally aren’t recognized as revenue until the condition is substantially met.

Example: Conditional grant vs. restricted gift

- Restricted: “Use this $50,000 (or donated equipment) for the summer youth program.” You can recognize it now, but it may be “with donor restrictions.”

- Conditional: “We’ll donate $50,000 worth of equipment if you raise matching funds by June 30, and if you don’t, we can cancel/require return.” You may need to wait.

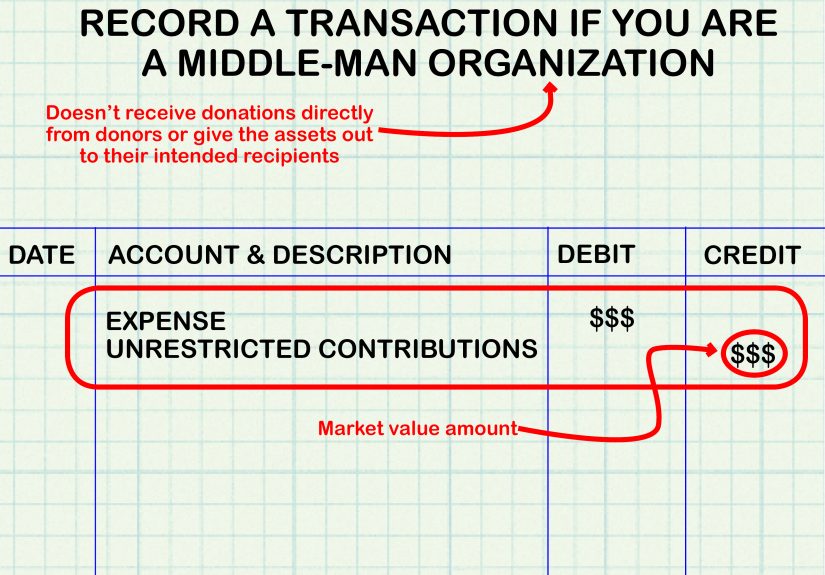

Tip 2: Recognize Donated Assets at Fair ValueThen Back It Up

For most donated noncash items, the starting point is recording the asset at fair value at the date of donation (the “measurement date”),

with a corresponding amount of contribution revenue. Fair value is not “whatever sounds nice” and it’s not necessarily what the donor paid. It’s a

market-based estimate of what you’d receive to sell the item (or what you’d pay to replace it) under reasonable assumptions.

Documentation that makes auditors relax their shoulders

- Donation receipt form with date received, description, condition, quantity, and intended use (use vs. sell).

- Valuation support (quoted prices, catalog screenshots, recent sales history, third-party appraisals for certain assets).

- Approval/review trail for the valuation (who estimated it, who reviewed it, and when).

If your valuation method is “we eyeballed it and the eyeball felt confident,” at least make it a repeatable eyeball: define a consistent process

(e.g., average of two public prices, or a standard thrift valuation grid).

Tip 3: Use the Right Journal Entry Pattern (Asset + Revenue, Often with Matching Expense)

The most common donated asset entry for a nonprofit looks like this:

Example: Donated supplies used in programs

When you use those supplies, you’ll also recognize expense (so the financials show both the gift received and the resources consumed):

This two-step approach keeps your balance sheet honest (you actually have supplies until you use them) and keeps expenses aligned with the period of use.

If you record everything directly to expense at receipt, it can be acceptable in some situations, but it may distort inventory/asset balancesespecially if

you receive large year-end donations.

Tip 4: Separate “Financial Assets” from “Nonfinancial Assets” in Your Reporting

Donated stock is not the same thing as donated food, and your statements should reflect that reality. Under newer

nonprofit presentation/disclosure expectations, you’ll often present contributed nonfinancial assets separately from contributions of cash and other

financial assets. Build your chart of accounts so you can report cleanly without a last-minute spreadsheet carnival.

Practical chart-of-accounts tweak

- Contribution Revenue – Cash

- Contribution Revenue – Donated Financial Assets (e.g., securities)

- Contribution Revenue – Donated Nonfinancial Assets (in-kind)

- Contribution Revenue – Donated Services (if recognized)

This structure makes year-end reporting more accurate and reduces the temptation to “just dump it into Donations and hope for the best.”

Tip 5: Treat Donated Securities Like InvestmentsBecause That’s What They Are

For publicly traded stock gifts, you generally record the investment at fair value on the date your organization receives control of it, with contribution

revenue. Then, when you sell, you recognize cash and any gain/loss based on the change in value since receipt.

Example: Donated stock (received then sold later)

Operational tip: If your policy is to sell immediately, you still want a consistent method for determining the fair value on the

receipt date (many organizations use the day’s quoted market price or an average of high/lowjust be consistent and document it).

Tip 6: Record Donated Fixed Assets (PPE) with a Plan for Depreciation and Restrictions

Donated equipment, vehicles, and buildings are not “free stuff you never think about again.” Once recorded at fair value, they usually live on your

balance sheet and get depreciated over their useful lives, just like purchased assets.

Example: Donated vehicle

Then you depreciate it over its useful life according to your capitalization and depreciation policy. If a donor restriction requires the asset be used

for a specific purpose (or not sold for a period), track the restriction in your donor-restriction system and disclosures as needed.

Best practice: Align your gift acceptance policy with your capitalization policy. If you wouldn’t capitalize a

$400 printer when purchased, don’t suddenly capitalize it because it arrived with a ribbon on top.

Tip 7: Donated Inventory for Resale Needs a “Use vs. Sell” Decision Up Front

Some donated goods are meant to be distributed (food pantry), and some are meant to be sold (thrift store). That decision affects classification and the

expense pattern.

If you will sell the items

- Record the donated items (inventory) at fair value at receipt when reasonably estimable.

- Recognize contribution revenue at receipt.

- Recognize cost of goods sold when sold (based on the recorded inventory value).

Example: Thrift store donation then sale

Yes, that means your thrift store can show gross margin even though the inventory was donated. That’s not a bugit’s the financial statement reflecting

that donated resources were converted into cash to fund mission.

Tip 8: Only Record Donated Services When They Meet Recognition Criteria

Volunteer hours are pricelessand also frequently not recorded in the financial statements. Under common nonprofit GAAP concepts, donated

services are recognized when they either (a) create or enhance a nonfinancial asset (like construction) or (b) require specialized skills, are provided by

someone with those skills, and would typically need to be purchased if not donated.

Examples

- Recordable: pro bono legal services, donated audit work, donated electrician labor renovating your facility.

- Usually not recorded: general volunteer time like stuffing envelopes, serving at events, basic administrative help.

Example entry: Donated legal services

Recording services correctly helps avoid overstating revenue (and mission impact) with estimates that aren’t supported by the rules or documentation.

Tip 9: Build a Repeatable Valuation Playbook (Not a “Valuation Mood Board”)

Valuation is where donated assets get messy. Your goal isn’t perfection; it’s a reasonable, consistent, well-supported method. Create a short written

playbook that answers:

- What market do we use? Retail replacement cost? Wholesale? Recent comparable sales?

- What condition adjustments apply? New, gently used, heavily used, “mysterious but functional.”

- Who estimates and who approves? Separation of duties helps.

- When do we require an appraisal? (Often for high-value or unusual items.)

Also: don’t confuse a donor’s “estimated value” with your organization’s accounting value. The donor’s number may be helpful context, but you still need

your own support.

Tip 10: Design Your Tracking for DisclosuresSo Year-End Isn’t a Treasure Hunt

Modern nonprofit reporting expectations often require more transparency for contributed nonfinancial assets. That means your system should capture donated

asset categories and key qualitative info as you go, not in a panic two days before the audit.

Data fields worth capturing at the moment of receipt

- Asset category (food, medical supplies, equipment, professional services, etc.)

- Whether the asset was monetized (sold) or used in programs

- Donor restrictions (time, purpose, use limitations)

- Valuation technique and inputs (quoted price, appraisal, internal grid, etc.)

- Principal market (where the valuation evidence comes from)

The secret to clean disclosures is boring operational discipline. The more consistent your tracking, the less you’ll rely on memory, guesswork, or that

one spreadsheet named “final_final2_REALLYFINAL.”

Common Recording Scenarios (Quick Examples)

Scenario A: Donated laptops used for a training program

Record laptops at fair value when received as equipment (or supplies) and recognize contribution revenue. If capitalized, depreciate over the useful life.

If expensed, document the rationale (materiality, policy threshold).

Scenario B: Donated food to a pantry

Record inventory at fair value when received (if reasonably estimable), then expense to program when distributed. Track pounds/units to support program

metrics separate from accounting valuation.

Scenario C: Donated construction services improving your building

If the services create or enhance a nonfinancial asset, record them as part of the asset cost (capitalized) and recognize contribution revenue for the

same amount.

Scenario D: Donated items intended for immediate sale

Record inventory and in-kind revenue at receipt; record sales and cost of goods sold upon sale. If items are immediately sold and the timing difference is

immaterial, your process may be simplerbut stay consistent and document your policy.

Real-World Experiences: What This Looks Like Outside a Textbook (About )

If you’ve ever tried to “quickly record in-kind donations,” you already know the universe responds by sending you the most complicated donation possible at

the worst possible time. One finance director told me their largest donated-asset month was Decemberbecause apparently generosity peaks precisely when

everyone’s out of office and your accounting team is living on holiday cookies and courage.

A common early-stage experience is the “single-bucket problem”: everything noncash goes into one general revenue account called something like “Donations.”

It worksuntil it doesn’t. The first time an auditor asks, “How much of this is donated goods versus donated services versus donated securities?” the room

gets quiet, and someone starts opening old emails like they’re searching for buried treasure. The fix is usually simple: create separate accounts and track

categories at intake. The hard part is the behavior change: getting program staff to capture details at receipt, not three months later when the item has

become “that box in the supply closet.”

Valuation is the second major “real life” hurdle. Many teams start with donor-provided values, then learn (sometimes abruptly) that donor values are not

always objective, consistent, or aimed at financial reporting. A donation form might say “10 laptopsvalue $15,000,” but a quick check shows they’re older

models with missing chargers. The best experience-based solution is building a valuation playbook that’s fair, consistent, and fastlike using a standard

depreciation grid for used electronics, or referencing two independent market listings for comparable items. The win isn’t just audit comfort; it’s internal

clarity. People stop arguing about numbers and start trusting the process.

Another recurring experience is the “in-kind whiplash” on statements: leaders see revenue jump and assume fundraising exploded, when the increase is mostly

donated goods that also created matching expense. The first time a board member asks, “Why did revenue rise but cash didn’t?” you get a teachable moment:

in-kind revenue can reflect real mission resources without adding cash. Experienced teams handle this by telling the story in management reportsshowing

cash vs. noncash contributions separately, and explaining how donated goods supported programs.

Finally, the best-run organizations treat donated assets as a cross-functional process, not an accounting afterthought. Programs document receipt and use;

operations confirms condition and storage; finance applies valuation and entry; leadership reviews policies. It’s not glamorous, but it’s the difference

between “We think we received a lot of stuff” and “We can prove what we received, how we valued it, and how it fueled our mission.” That kind of clarity

doesn’t just satisfy auditorsit builds donor trust.

Conclusion: Make Donated Assets Boring (In the Best Way)

Donated assets should feel like support, not suspense. When you classify the transaction correctly, value it consistently, record it with the right entry

pattern, and track the details needed for reporting, you turn “in-kind chaos” into clean, defensible financial statements. The bonus is strategic: you can

explain to donors and stakeholders exactly how noncash gifts strengthen your workwithout hand-waving, scrambling, or pretending that a donated couch is the

same as a cash grant.

Use the 10 tips as your baseline, then refine your policies as your organization grows. And remember: the goal isn’t to make accounting exciting. The goal

is to make it reliable. Excitement is for fundraising galas and rescue puppiesnot year-end adjusting entries.