Table of Contents >> Show >> Hide

- The Original Roaring Twenties: A Party After Deep Pain

- Step One: The Great Recession Changes the Rules (2008–2012)

- Step Two: A Long, Uneven Expansion and a Mountain of Risk-Taking (2013–2019)

- Step Three: A Pandemic Shock and the Biggest Policy Firehose in History

- Step Four: From Crisis to the “Roaring 2020s”

- What Really Drove the Modern Roaring Twenties?

- Common-Sense Lessons from Our Roaring 2020s

- Conclusion: Enjoy the Ride, but Don’t Forget the Seatbelt

- SEO Wrap-Up

- Extra: Real-World Experiences from Our Modern Roaring Twenties

If you had told anyone in March 2020when the world was stockpiling toilet paper and doomscrollingthat a few years later we’d be talking about a new version of the “Roaring Twenties,” they probably would’ve laughed, cried, or both. Yet here we are: markets near record highs, house prices way up, travel booming, restaurants packed, and investors arguing about whether this is all genius policy…or a bubble with better Wi-Fi.

So how did we get from global crisis to something that, at least on the surface, looks like a modern Roaring 2020s? To answer that, you need a little history, a little economics, and a big dose of common sensevery much in the spirit of the

A Wealth of Common Sense blog that helped popularize this comparison.

Let’s walk through the story: from the original Roaring Twenties a century ago, to the Great Recession, to COVID-19, and finally to the strange, booming, slightly surreal economy we’re living in today.

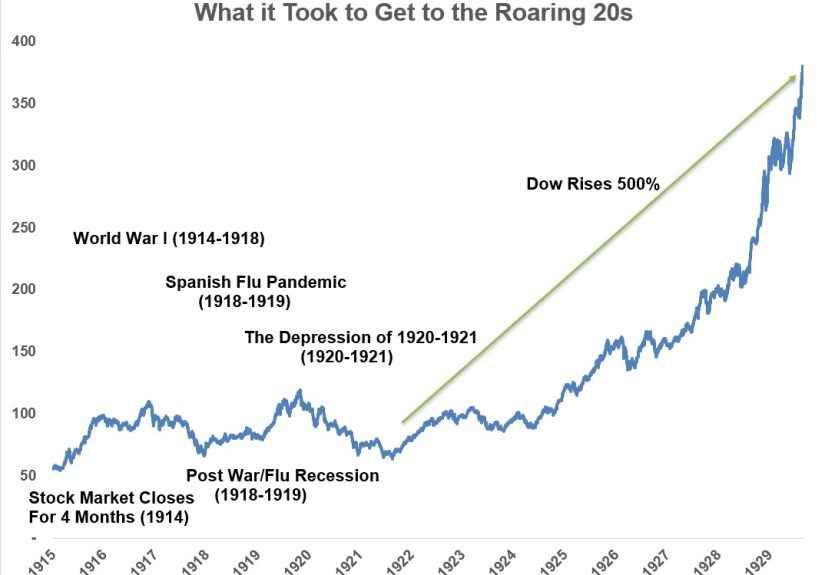

The Original Roaring Twenties: A Party After Deep Pain

When people talk about the “Roaring Twenties,” they usually mean the 1920s in the United States: jazz, flappers, speakeasies, stock-market speculation, and rapid technological change. But that decade didn’t come out of nowhere. It followed:

- World War I, with massive human and economic losses

- The 1918–1919 influenza pandemic

- A short but nasty recession in the early 1920s

In other words, the party came after a long stretch of trauma and uncertainty. Once the war and the flu faded, pent-up demand for normal life exploded. People wanted to travel, spend, dance, and invest. New technologiescars, radio, home appliancesmade it easier to enjoy rising incomes and modern comforts.

Easy credit also fueled the boom. Borrowing to buy stocks became common, and optimism turned into euphoria. That didn’t end well: the stock market crash of 1929 and the Great Depression slammed the brakes on the fun. But the pattern matters: deep crisis, massive behavioral shifts, and then a powerful (if unstable) boom.

Sound familiar yet?

Step One: The Great Recession Changes the Rules (2008–2012)

Fast-forward to the late 2000s. The housing bubble popped, major banks teetered, and the global financial system almost collapsed. The Great Recession (2007–2009) was the worst downturn since the 1930s. Millions of Americans lost jobs and homes, and the recovery was painfully slow.

To keep the financial system from imploding, the Federal Reserve and other central banks slashed interest rates to near zero and launched something that once sounded exotic: quantitative easing (QE), large-scale purchases of bonds and other securities. The goal was simple: keep borrowing costs low, support lending, and prevent a deflationary spiral.

These policies worked in the sense that they stabilized the system and eventually helped the economy recover. But they also set the stage for what came next:

- Persistently low interest rates: Safe assets like cash and bonds offered tiny returns, pushing investors into stocks, real estate, and other riskier assets.

- Rising asset prices: Stocks and housing gradually recovered, then climbed far beyond pre-crisis levels over the 2010s.

- Growing inequality: Households that owned financial assets and property saw their wealth rise, while many others were still digging out from job losses and foreclosures.

The result was a kind of “quiet bull market.” The economy grew, but it never felt like a party for everyone. It was more like a cautious dinner where the wealthy ordered dessert and everyone else checked their bank apps.

Step Two: A Long, Uneven Expansion and a Mountain of Risk-Taking (2013–2019)

By the mid-2010s, something odd was going on. We had:

- One of the longest economic expansions on record

- Very low inflation, despite all the money created by central banks

- Persistently low interest rates and several rounds of QE in the U.S. and abroad

Investors and companies adapted. When “cash is trash” becomes a slogan, you know the environment has shifted. With borrowing so cheap, it made sense to:

- Refinance debt at low rates

- Buy back shares to boost stock prices

- Fund high-growth, low-profit companies in tech and beyond

At the same time, the growth of index funds, robo-advisors, and automatic enrollment in retirement plans put more households into the market, whether or not they thought of themselves as “investors.” Wealth creation started to track market performance more tightly than wage growth.

Underneath the surface, inequality widened. The top of the wealth distribution gained from rising stocks and home values, while many people were still just trying to keep up with rent, healthcare, and student loans. But as long as inflation stayed low and markets marched upward, the system held together.

Then came 2020.

Step Three: A Pandemic Shock and the Biggest Policy Firehose in History

The COVID-19 pandemic hit like a meteor. In early 2020, economic activity fell off a cliff. Businesses shut down. Unemployment exploded in weeks. For a brief moment, it looked like the Great Depression might be making a comebackbut with Zoom meetings.

Policymakers, having lived through the Great Recession, responded in a completely different way this time. Instead of cautious, incremental moves, they turned on the firehose:

- Interest rates: The Fed slashed rates back to near zero almost immediately.

- Massive QE: The central bank bought huge amounts of government bonds and mortgage-backed securities to keep markets functioning.

- Fiscal stimulus: Congress approved several trillion dollars in aiddirect checks to households, enhanced unemployment benefits, forgivable loans for small businesses, and more.

Because people were stuck at home, they couldn’t spend on normal services like travel, dining out, or entertainment. At the same time, government support actually boosted many households’ incomes. The result was a surge in savings, often referred to as “excess savings”trillions of dollars more than people would’ve accumulated under pre-pandemic trends.

When the economy reopened, all of that purchasing power went looking for a home. Some of it went into:

- Stocks: A roaring bull market emerged after the brief “corona crash.” Retail trading platforms surged in popularity, and meme stocks became cocktail-party conversation.

- Housing: Remote work, low mortgage rates, and cash from stimulus and savings fueled a historic house-price boom.

- Crypto and speculative assets: When people have extra cash and boredom, “number go up” becomes a surprisingly powerful narrative.

This is where the “Roaring 2020s” analogy really starts to make sense. Just as the 1920s were fueled by new technologies and easier credit, the 2020s saw cheap money, massive stimulus, and digital platforms that made speculation as easy as tapping an app.

Step Four: From Crisis to the “Roaring 2020s”

As the pandemic shock faded, the U.S. economy did something economists don’t always see: it bounced back fast. Jobs returned faster than many forecasts expected. Corporate profits rebounded. Consumers spent heavily, especially on travel, entertainment, and goods that had been out of reach during lockdowns.

At the same time, all that demand hit supply chains that were still tangled. The result? The highest inflation in decades. To fight it, the Fed raised interest rates at one of the fastest paces in modern history.

Normally, such aggressive rate hikes would slam the brakes on growth and markets. But thanks to:

- Earlier gains in household wealth from rising stocks and home prices

- Still-elevated savings for many upper-income households

- Strong corporate balance sheets and profits in key sectors

The economy kept chugging along. High-income consumers, in particular, continued to spend on travel, premium services, and experiences. Asset holdersthose owning stocks, real estate, and other investmentsbenefited from the rebound in markets after each scare.

This is the strange mix we see today: strong consumer spending, high asset prices, and unemployment that’s low by historical standards, coexisting with very real affordability struggles for people who rent, earn lower wages, or don’t own assets. The “Roaring 2020s” feel great if your portfolio and home equity are booming; they feel very different if you’re on the outside looking in.

What Really Drove the Modern Roaring Twenties?

If we boil it down, how did we ever get to these new Roaring Twenties? Think of four big forces working together:

1. Ultra-low Interest Rates and Quantitative Easing

More than a decade of low rates made borrowing cheap and pushed investors toward riskier assets. QE suppressed yields on safer bonds, encouraging a “reach for yield” across the system. Over time, that helped inflate asset prices and rewarded those who already owned stocks and real estate.

2. Massive Fiscal Stimulus During the Pandemic

The speed and scale of pandemic relief were unprecedented. Direct payments, expanded unemployment benefits, and business support programs didn’t just prevent a depression; they injected huge amounts of cash into the economy. That supported demand, increased savings for many households, and later helped fuel spending and investment.

3. Technology and Frictionless Speculation

Smartphone apps, commission-free trading, social-media amplification, and 24/7 financial content turned markets into a kind of always-on entertainment. Retail investors could buy stocks, options, and crypto in seconds. That’s powerful in any environmentbut when combined with stimulus money and boredom, it supercharged speculative behavior.

4. Wealth Effects and Inequality

As asset prices climbed, households that owned financial assets or real estate saw their net worth rise significantly. That “wealth effect” supported ongoing spending, especially among older and higher-income households. But it also widened the gap between people who benefit from markets and those who don’t, creating a two-track economy.

Together, these ingredients built a world where markets can have huge swings, but the overall trend has been surprisingly resilient. It’s not a party for everyonebut from the perspective of asset prices and economic data, it really does look like a new roaring era.

Common-Sense Lessons from Our Roaring 2020s

The temptation, in any boom, is to assume “this time is different” and let FOMO drive your decisions. A more common-sense approachtrue to the spirit of

A Wealth of Common Sensewould be to draw a few grounded lessons:

- Big booms usually follow big traumas. The 1920s followed war and pandemic; the 2020s followed financial crisis and another pandemic. When people have been constrained, their desire to spend, invest, and take risk often snaps back hard.

- Policy choices matter. Low rates, QE, and stimulus checks weren’t background noise; they were central drivers of the recovery and the boomand they shaped who gained the most.

- Wealth isn’t evenly distributed. When asset prices soar, owners of those assets pull further ahead. That creates both opportunities (if you’re invested) and real social and political tensions (if you’re not).

- Cycles don’t last forever. The original Roaring Twenties ended in a crash. That doesn’t mean history will repeat exactly, but it’s a reminder that euphoria and high valuations can make the system fragile.

- Humility is a superpower. It was hard to predict the crash in early 2020, even harder to predict the speed of the recovery, and nearly impossible to time each twist and turn. Having a long-term plan matters more than calling every cycle perfectly.

Conclusion: Enjoy the Ride, but Don’t Forget the Seatbelt

The question “How did we ever get to the Roaring Twenties?” has a surprisingly simple answer: we layered extraordinary policy responses on top of deep crises, in a world already primed by years of low interest rates and rising inequality. When the dam finally broke, all that money, innovation, and pent-up demand rushed into the real economy and financial markets at once.

The result is the world we see today: vibrant, volatile, and unequal. Some people feel like they’re living in a golden age of opportunity; others feel like they’re running on a treadmill that keeps speeding up. Both perspectives can be true.

The common-sense takeaway isn’t to panic or to party endlesslyit’s to recognize that booms are part of long cycles, not permanent conditions. Use the good times to shore up your finances: pay down expensive debt, invest consistently, keep some liquidity, and avoid betting your future on a story that only works if everything keeps roaring forever.

History suggests there will be more crashes, more recoveries, and more unexpected turning points. But if you approach the Roaring 2020s with clear eyes, a long-term plan, and a little humility, you don’t have to predict the future perfectly to end up okay.

SEO Wrap-Up

sapo:

From the Great Recession to COVID-19 and beyond, the path to our modern “Roaring 2020s” has been anything but straight. Years of ultra-low interest rates, repeated rounds of quantitative easing, and trillions in pandemic stimulus quietly rewired how money, markets, and everyday people interact. When the world finally reopened, pent-up demand and record savings collided with powerful technology and frictionless trading platforms, driving a surge in asset prices and consumer spending. This article breaks down how we got here, why the boom feels so different depending on your income and wealth, and what common-sense investors can learn from both the original Roaring Twenties and our high-volatility, high-uncertainty 2020s era.

Extra: Real-World Experiences from Our Modern Roaring Twenties

It’s one thing to talk about the Roaring 2020s in charts and economic jargon; it’s another to feel it in everyday life. For many people, the last few years have looked like a mash-up of a finance textbook and a reality showpart opportunity, part chaos, part “wait, is this normal?”

Think about the young professional who started investing in 2019 with a modest index fund contribution. They watched their account nosedive during the 2020 crash, then roar back with unbelievable speed. By 2021, their balance was not only back but hitting new highs. The emotional whiplashfear, relief, then cautious optimismchanged how they thought about risk. They didn’t become a full-time day trader, but they did become someone who logs into their brokerage app a lot more than their grandparents ever did.

Or take the couple who bought a home right before the pandemic, mostly because their rent felt like setting money on fire each month. At the time, the mortgage payment seemed like a stretch. Just a few years later, they looked up and realized that similar homes in their neighborhood were selling for eye-watering prices. Their monthly payment stayed the same, but their home equity ballooned. Suddenly, they weren’t just “homeowners”; they were “sitting on a major asset.” That shift didn’t change their day-to-day lives overnight, but it did alter how secure they felt and how they thought about retirement.

On the flip side, consider renters in those same booming housing markets. As home prices and interest rates climbed, landlords pushed rents higher to keep up. For them, the Roaring 2020s didn’t feel like a wealth-building era; it felt like a constant scramble not to fall behind. Raises at work were swallowed by rent increases, childcare costs, and groceries. They watched stock-market records and real-estate headlines with a mix of curiosity and frustration, feeling like the party was happening somewhere else.

There’s also the story of the pandemic entrepreneur. Millions of people used lockdown as a forced reset and finally launched the side hustles and small businesses they’d been dreaming about: online stores, consulting gigs, content channels, specialty food brands, and more. For some, stimulus money and extra time at home removed just enough friction to take the leap. The combination of cheap digital tools, social-media marketing, and global reach allowed small players to punch way above their weight. A few of these ventures flopped, a few grew into serious companies, and many settled into that surprisingly powerful middle grounda sustainable small business that never would’ve existed without the strange conditions of 2020–2022.

If you zoom out from these individual experiences, a pattern emerges. People who had some combination of:

- Access to capital or steady income

- Ownership of assets like homes or retirement accounts

- Flexibility to work remotely or change careers

often found ways to ride the wave of the Roaring 2020s. They may not feel “rich,” but they’ve seen real gains in wealth, stability, or opportunity. For othersespecially those with unstable jobs, no cushion of savings, or no asset ownershipthe same period has felt like an exhausting obstacle course.

That tension is exactly why a common-sense approach is so important. You don’t control interest rates, government policy, or global pandemics. You do control whether you:

- Build even a small emergency fund when times are good

- Invest regularly instead of trying to guess turning points

- Avoid chasing the loudest speculation just because it’s trending

- Think about housing, debt, and career decisions as part of one big life plan, not separate silos

Living through the Roaring 2020s doesn’t require you to predict the next big macro move. It asks something simpler and harder: to stay level-headed when the world swings between panic and euphoria. If you can keep showing up, saving consistently, and making patient choiceseven while the headlines screamyou’re already practicing the kind of wealth management that truly earns the label “a wealth of common sense.”