Table of Contents >> Show >> Hide

- What “Defying the Fed” Actually Means

- Why Markets Can Overrule the Message

- The Classic Episodes: When Markets Didn’t Take the Hint

- How the Fed Pushes Back (Without Picking a Bar Fight)

- How to Tell If Markets Are Rightor Just Loud

- Why This Tug-of-War Matters for Everyone

- Experiences When Markets Defy the Fed

- Conclusion

The Federal Reserve is supposed to be the main character in the interest-rate story. It sets the policy rate, holds press

conferences, and releases projections with more dots than a kindergarten art class. And yetevery so oftenmarkets shrug,

grin, and do whatever they want.

That’s the moment people describe as “markets defying the Fed”: when investors price a future that doesn’t match

the Fed’s message, and financial conditions move in the “wrong” direction. The Fed says “higher for longer,” and bond yields

drop. The Fed signals patience, and markets panic anyway. It’s like the referee calling a timeout while the crowd keeps

chanting, “Play on!”

What “Defying the Fed” Actually Means

The Fed speaks; markets price a different future

The Fed controls a very specific lever: the federal funds rate (an overnight rate in money markets). But investors trade

everything elseTreasury yields across maturities, mortgage rates, corporate credit spreads, and stock valuationsbased on

where they believe the economy and policy are headed.

When markets “defy” the Fed, they’re not staging a revolution against the marble columns in Washington. They’re expressing a

different forecast. If investors believe inflation will cool faster than the Fed expects, they’ll price earlier rate cuts.

If they believe growth is about to slip, they’ll buy longer-term Treasuries, pushing those yields downeven if the Fed is

still hiking.

Two markets, two jobs: overnight policy vs. long-term reality

Think of the fed funds rate as the Fed’s steering wheel. It’s importantbut it doesn’t decide how bumpy the road is. Longer-term

interest rates reflect expectations about future short rates and the broader economy over years, not days. That means markets can

“win” the long end of the curve even if the Fed “wins” the next meeting.

Why Markets Can Overrule the Message

Expectations: the market is always living in the future

A big chunk of any long-term yield is basically a forecast: where short-term rates will average over time. If traders revise

that forecastbecause inflation data softened, job growth slowed, or recession risks roselonger-term yields can move in ways

that contradict the Fed’s current tone.

This is why markets sometimes rally on “bad news.” A weaker jobs report can push investors to expect fewer hikes (or faster cuts),

lowering yields and boosting stocks. It’s not that investors love bad economic outcomes; it’s that they love the idea of a less

restrictive rate path. Yes, it’s weird. No, it’s not new.

Term premium: the extra ingredient in long yields

Even if everyone agreed on the expected path of short rates (they don’t), long-term yields also include something called the

term premium: extra compensation investors demand for locking money up for longer periods amid uncertainty.

Term premia can change for reasons that have little to do with the Fed’s next move: shifts in risk appetite, demand from pension

funds and global investors, volatility in inflation, or worries about government borrowing. That’s how the Fed can be hiking while

the 10-year yield drifts lowermarkets may simply be accepting a smaller premium for duration risk (or chasing safety).

Global money and fiscal supply: “It’s not just you, Fed”

U.S. markets are global markets. Foreign demand for Treasuries, changes in overseas rates, and currency-hedging costs can all

shape yields. Meanwhile, the U.S. government’s borrowing needs can affect how much Treasury supply the market must absorb.

Sometimes the long end is reacting to global growth fears, geopolitics, or supply-and-demand mathnot the Fed’s preferred

narrative arc.

Financial conditions: stocks, credit, and the “vibes index”

Central bankers watch more than the policy rate. They also watch financial conditionsa broad mix of yields, stock

prices, credit spreads, and volatility that influences the real economy. When stocks surge, spreads tighten, and borrowing looks

easy, financial conditions loosen. That can make it harder for the Fed to cool inflation, even if the policy rate is high.

The twist: different financial-conditions indexes can sometimes tell different stories, depending on what they emphasize and how

they’re built. So even the “vibes index” comes with fine print.

The Classic Episodes: When Markets Didn’t Take the Hint

1) Greenspan’s “conundrum”: hiking… while long yields fell

One of the most famous “Fed versus market” moments came during the mid-2000s tightening cycle. The Fed raised short-term rates,

yet longer-term Treasury yields didn’t rise as much as expectedand at times moved lower. Alan Greenspan called the behavior of

bond markets a “conundrum,” highlighting how global savings, inflation credibility, and term-premium dynamics can mute the usual

policy transmission.

Translation: the Fed was pressing the brake, and the bond market was calmly saying, “Cool, but we think the car is already slowing.”

2) The 2013 taper tantrum: markets ran ahead of the plan

In 2013, mere discussion of slowing (“tapering”) asset purchases sparked a sharp move in yields and volatility. The Fed hadn’t

actually reduced purchases yet; markets reacted to the idea and the communication shift. This episode was a reminder that

policy isn’t just what the Fed doesit’s what investors believe it’s about to do.

The tantrum also showed how sensitive markets can be to balance-sheet policy and forward guidance, especially after years of

quantitative easing made investors feel like the Fed was the unofficial sponsor of risk-taking.

3) 2018: “Long way from neutral” and the whiplash

In October 2018, Chair Jerome Powell remarked that policy was “a long way from neutral,” a phrase markets interpreted as more

hawkish than expected. Risk assets wobbled. Later, communication shiftedPowell described rates as “just below” neutraland

markets took it as a sign the Fed might be closer to pausing. The lesson wasn’t that one phrase controls the world; it was that

when expectations are fragile, wording can be a match near a gasoline can.

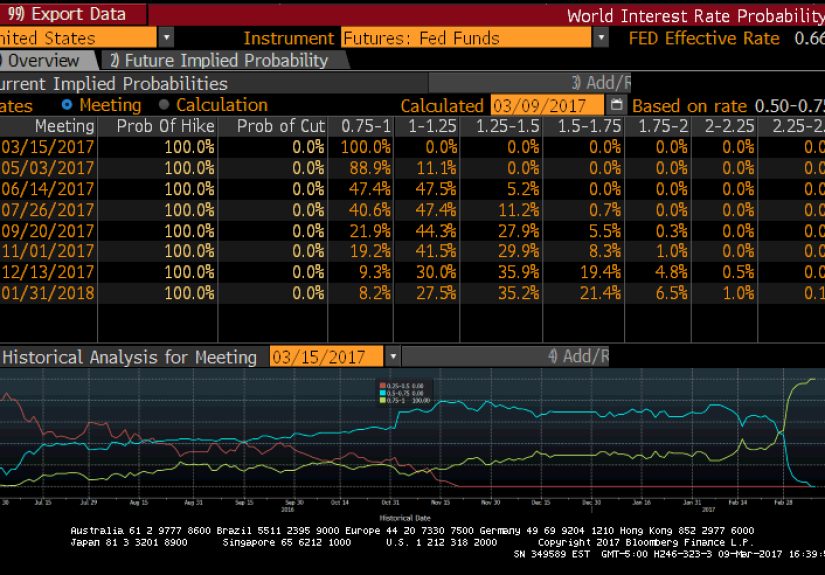

4) The modern pattern: markets front-run cuts while the Fed talks tough

In more recent cycles, it’s common to see a push-and-pull: the Fed emphasizes being “data dependent” and keeping policy restrictive

until inflation is convincingly on track, while markets price earlier cuts based on slowing indicators or recession risk.

This is where “defiance” usually shows up in everyday commentary: bond yields fall, stocks rally, and traders say the market “doesn’t

believe” the Fed. Sometimes the market is right. Sometimes it’s just earlylike showing up to a party before the host has finished

cleaning. Awkward for everyone.

How the Fed Pushes Back (Without Picking a Bar Fight)

1) Forward guidance and “higher for longer” storytelling

The Fed uses communication to shape expectations because expectations are part of how policy works. If markets loosen too much

(yields down, stocks up), the Fed may respond with hawkish language: emphasizing inflation risks, reminding everyone that cuts

aren’t imminent, and repeating variations of “we’ll do what it takes.”

2) Balance sheet tools: the plumbing matters

Quantitative easing (QE) and quantitative tightening (QT) can influence longer-term yields, liquidity, and term premia. Even when

the policy rate is unchanged, changes in the Fed’s balance sheet can move marketsespecially those sensitive to Treasury supply,

volatility, and risk appetite.

3) Credibility and the “reaction function”

Markets spend a lot of energy trying to decode the Fed’s reaction functionhow policymakers respond to inflation, employment,

financial stability risks, and growth. If investors think the Fed will blink at the first sign of weakness, markets may price

earlier easing. If investors think the Fed is determined to protect its inflation credibility, markets may accept higher rates

for longer. In a sense, “defiance” is often a referendum on credibility.

How to Tell If Markets Are Rightor Just Loud

Watch the trio: inflation, jobs, and growth

The cleanest way to understand the clash is to ask: what data would justify the market’s path versus the Fed’s path?

If inflation is cooling, wage growth is moderating, and demand is slowing, the market’s “cuts sooner” story strengthens.

If inflation reaccelerates or demand stays hot, the Fed’s “stay restrictive” story looks smarter.

Look under the hood: credit spreads and term premia

A rally driven by lower term premium and improved inflation confidence looks different than a rally driven by pure risk-on exuberance.

Credit spreads (the extra yield companies pay over Treasuries) can be revealing. If spreads are tight while equities soar, financial

conditions may be loosening meaningfully. If spreads widen while Treasuries rally, markets may be sniffing out growth trouble.

Compare multiple financial-conditions indexes

Financial conditions aren’t a single number carved into stone tablets. Different indexes weight components differently, which can

lead to disagreements about whether conditions are “tight” or “loose.” Cross-checking more than one measure can help you avoid

overreacting to a single dashboard reading.

Why This Tug-of-War Matters for Everyone

Mortgages, car loans, and business borrowing

Most people don’t borrow at the fed funds rate. They borrow at rates linked to longer-term yields and credit spreads. When markets

“defy the Fed” by pushing long rates down, mortgage rates can fall even if the Fed hasn’t cut. When markets panic, borrowing costs

can rise quickly even if the Fed is steady.

Retirement accounts and risk appetite

Equity valuations are sensitive to discount rates and growth expectations. If markets conclude the Fed will ease sooner, stocks

can rallysometimes sharply. If markets conclude the Fed will stay restrictive, or that growth is weakening, risk assets can

reprice fast. That’s why this drama isn’t just for traders in vests yelling at screens. It shows up in 401(k)s and college

savings plans too.

The “soft landing” storyline

The happiest version of “markets defy the Fed” is when investors anticipate disinflation and a gentle slowdownso yields fall

and stocks stay supported. The grumpiest version is when yields fall because markets expect a hard landing. Same direction in

rates, totally different reason. Context is everything.

Experiences When Markets Defy the Fed

If you want to understand this topic in human terms, skip the jargon for a minute and look at how it feels in real lifebecause

“markets defy the Fed” isn’t just a headline. It’s a sequence of tiny shocks that ripple through decisions people have to make.

Consider the homebuyer who’s been refreshing mortgage-rate quotes like it’s concert-ticket day. The Fed holds rates steady and

sounds tough in a press conference, but the next week mortgage rates dip anyway because long-term Treasury yields slid on a softer

inflation print. Suddenly, the buyer’s lender calls with a cheery “Want to lock today?” The buyer doesn’t care about term premia

or forward guidance; they care that a monthly payment just moved by a meaningful amount. That’s the market doing the real-world

transmissionsometimes faster than the Fed would prefer.

Or take a small-business owner planning to finance new equipment. They hear “higher for longer” and brace for pain. Then a

surprise market rally tightens credit spreads and lenders compete harder for loans. Rates offered to the business improve even

without a Fed cut. The owner thinks, “Wait, I thought borrowing was supposed to get harder.” Welcome to the part where markets

interpret the future and start implementing it early.

On the institutional side, portfolio managers live inside this tug-of-war. A bond manager might watch the Fed project fewer cuts

than futures markets imply, then ask: “Is the market seeing recession risk the Fed isn’t emphasizingor is it just wishful

thinking priced as certainty?” Meanwhile, equity investors might celebrate falling yields as a reason to buy growth stocks, while

macro investors warn, “Falling yields can also be a smoke alarm.” The same chart becomes two different stories depending on which

economic movie you think you’re watching.

Even corporate finance teams feel it. A CFO trying to issue bonds learns that timing matters as much as fundamentals. If markets

decide the Fed will pivot, demand for corporate bonds can surge, lowering borrowing costs. Companies may rush to refinance, and

that wave of issuance can then change spreads again. It’s a feedback loop: markets anticipate easier policy, conditions loosen,

economic activity gets support, and the Fed may respond by sounding tougherbecause conditions loosened.

And then there’s the whiplash experience: one phrase in a speech, one unexpected data release, one geopolitical headlinesuddenly

the “rate path” everyone believed in gets redrawn. People who don’t think of themselves as “market participants” still experience

the consequences through loan offers, investment balances, and the general mood music of the economy. That’s why the phrase

“markets defy the Fed” sticks around. It captures a simple truth: the Fed drives policy, but markets drive pricesand prices

can change your life before the next FOMC meeting even starts.

Conclusion

When markets defy the Fed, it’s rarely pure rebellion. It’s usually the bond and stock markets doing what they always do:

translating messy, real-time information into a forecastand then trading on it. Sometimes that forecast is prescient. Sometimes

it’s premature. Either way, the tension matters because it shapes financial conditions, and financial conditions shape the

economy the Fed is trying to manage.

If you remember one thing, make it this: the Fed controls a short rate, but the market controls expectations. And expectations

are powerful enough to move mortgages, business borrowing, and portfolioseven while policymakers are still choosing their next

sentence.