Table of Contents >> Show >> Hide

- First, a reality check: bottoms are obvious only in hindsight

- The anatomy of a bottom: what you’ll usually see

- 1) Capitulation vibes: the “get me out at any price” moment

- 2) Volatility spikes, then starts calming down

- 3) Breadth improves: fewer stocks are collapsing under the surface

- 4) Credit spreads stop widening: stress in the “plumbing” eases

- 5) Sentiment hits extremes: everyone feels smart for being pessimistic

- 6) Price action flips from “sell the rip” to “buy the dip”

- False bottoms: why the market loves messing with your confidence

- Historical bottom “looks” (without pretending history repeats perfectly)

- So… how do you use this without turning into a chart detective?

- Common misconceptions about market bottoms

- A quick, practical “bottom spotting” framework

- Investor experiences: what a bottom feels like in real life (about )

- Conclusion

If you’ve ever tried to “spot the bottom” in the stock market, you already know the cruel joke:

the bottom only looks obvious after it’s behind youlike realizing you were in a bad haircut era

once you see the photos.

In real time, a bottom is less like a single magic candle on a chart and more like a process:

fear peaks, selling pressure gets exhausted, buyers slowly (then suddenly) show up, and the market starts acting

like it wants to live again. The trick is that the market is fully capable of staging dramatic “I’m back, baby!”

rallies… and then faceplanting a week later. So the goal isn’t to be a psychic. It’s to recognize the

cluster of signals that typically shows up when the selling is running out of oxygen.

Let’s break down what stock market bottoms often look likefrom price action and sentiment to credit markets and

economic cluesusing plain English, a little humor, and the kind of practical examples you can actually use.

First, a reality check: bottoms are obvious only in hindsight

A true market bottom is the lowest point before a sustained uptrend. That’s the textbook definition. The lived

experience is messier: a bottom can take the form of a sharp V-shaped rebound, a sloppy multi-month base, or a

“double bottom” where the market revisits lows and refuses to go lower.

Because of that, many professionals don’t try to nail the exact low. They look for a shift in behavior:

the market stops getting punished for good news, stops rewarding bad news, and starts rotating into healthier

internals (breadth, leadership, and risk appetite).

The anatomy of a bottom: what you’ll usually see

1) Capitulation vibes: the “get me out at any price” moment

Many major lows feature some flavor of capitulationa stretch where investors dump positions

to stop the pain. It doesn’t always look like one cinematic crash day; sometimes it’s a grinding surrender where

every rally gets sold and optimism becomes socially unacceptable.

Common tells:

- Big down days that feel emotional, not analytical.

- Headlines that use words like “panic,” “bloodbath,” or the always-classy “rout.”

- Volume jumps as people hit the eject button at once.

- “Nothing matters anymore” talkwhere even good companies get sold because cash feels like a hug.

Important nuance: capitulation is a possible ingredient, not a guarantee. Some bottoms are quiet and

boringmore like a car slowly running out of gas than a movie explosion.

2) Volatility spikes, then starts calming down

Volatility tends to surge when fear peaks. Think of it as the market’s pulse racing. A classic bottoming pattern

is: volatility spikes during the selloff, then stops making new highs even if prices retest lows.

That “fear is no longer escalating” detail can matter.

What a healthier post-panic setup often looks like:

- Volatility stops spiking on every down day.

- Market drops become less chaotic and more “orderly.”

- Rallies stop getting instantly slapped back down.

No, this doesn’t mean volatility must be low. It means volatility is no longer surprising the market every day.

3) Breadth improves: fewer stocks are collapsing under the surface

Indexes can be misleading. A handful of mega-stocks can hide a lot of damage, and they can also hide early healing.

That’s why investors watch market breadthhow many stocks are participating in the move.

Bottoms often form when internal selling pressure starts to fade:

- New lows dry up (fewer stocks are making fresh 52-week lows).

- Advance/decline measures stop deteriorating and begin to stabilize.

- The percentage of stocks above key moving averages starts improving.

A classic “the patient is no longer getting worse” sign: the index retests lows, but fewer stocks

make new lows the second time. That’s a divergence that can hint at exhaustion in selling.

4) Credit spreads stop widening: stress in the “plumbing” eases

Stocks get the attention, but credit markets often act like the market’s nervous system. When investors get scared,

they demand more compensation to hold riskier corporate debt. That shows up as wider credit spreads.

A common bottoming ingredient is not just “stocks bounce,” but “credit stress eases”:

- High-yield spreads stop widening aggressively.

- Financing conditions look less apocalyptic.

- “Risk-on” assets stop behaving like they’re all allergic to each other.

Translation: when the bond market stops screaming, equities often find it easier to stand up without immediately

falling over.

5) Sentiment hits extremes: everyone feels smart for being pessimistic

Sentiment indicators can be useful because markets are forward-looking. When nearly everyone is bearish,

a lot of selling may already be “used up.”

Signs the crowd has gotten emotionally exhausted:

- Surveys show unusually high bearishness.

- Put activity swells relative to call activity (fear hedging goes mainstream).

- Investors talk more about “getting back to even” than “making money.”

Contrarian logic isn’t magic. It’s a probability game: when pessimism is extreme, it can take surprisingly little

good news to push prices higher.

6) Price action flips from “sell the rip” to “buy the dip”

Here’s the most practical clue: at some point, the market stops rewarding bears for being right.

During the downtrend, you’ll often see:

- Rallies get sold quickly.

- Support levels break like cheap plastic.

- Good news gets ignored.

Near a bottom, behavior can change:

- Bad news stops pushing prices to fresh lows.

- Stocks start holding gains after earnings (even if guidance isn’t perfect).

- The market begins forming higher lows instead of relentless lower lows.

In other words, the market starts acting like it has buyers with convictionnot just day traders playing hot potato.

False bottoms: why the market loves messing with your confidence

Bear markets are famous for violent rallies. They happen because positioning is defensive,

short interest builds, and any whiff of relief can trigger sharp upside moves.

A “false bottom” often features:

- A strong rally that doesn’t fix breadth (the index rises, but most stocks still look sick).

- Credit spreads remain wide or keep widening.

- Leadership stays defensiveutilities and staples look “best,” while economically sensitive stocks still struggle.

- Economic data keeps deteriorating, and earnings estimates keep getting revised down.

This is why many investors look for confirmation instead of trying to catch the exact low.

Confirmation can mean a second higher low, improving participation, or a sustained break of a downtrend.

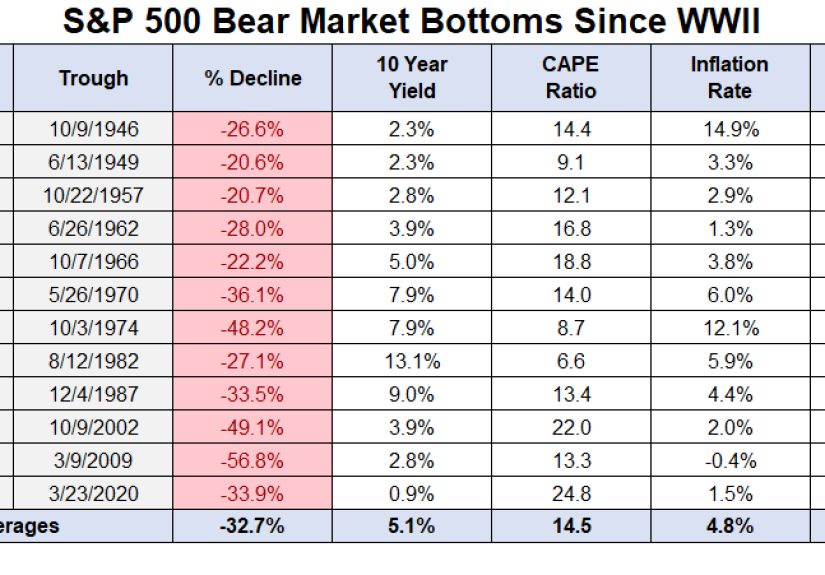

Historical bottom “looks” (without pretending history repeats perfectly)

The waterfall bottom: fast crash, fast response

Some bottoms happen after a rapid declinepanic selling, forced liquidations, then a swift rebound once selling

pressure burns off and policy or liquidity improves. These episodes often feature huge daily moves and a quick

shift from “the world is ending” to “wait, maybe not today.”

What typically matters most here is the exhaustion of forced selling and a clear catalyst that

changes the liquidity narrative.

The grinding bottom: long pain, then quiet healing

Other bottoms are slow. The market chops around, rallies fail, pessimism becomes a personality trait, and then

almost annoyinglystocks start rising before the news “feels” better.

In these environments, you’ll often see improvements in:

- breadth and leadership (more stocks participate),

- earnings revisions stabilizing,

- credit conditions gradually easing.

The double bottom: the retest that decides the trend

A common bottoming shape is a retest: the market revisits prior lows and either undercuts them briefly (to shake

out weak hands) or holds above them. If internals are healthier on the retestfewer new lows, better breadth,

calmer volatilitythat can be a meaningful tell.

So… how do you use this without turning into a chart detective?

Build a “weight of the evidence” checklist

Instead of betting your retirement on one indicator, use a scorecard. A bottom becomes more plausible when several

pieces line up. For example:

- Sentiment: bearishness is extreme, and fear looks “spent.”

- Volatility: spikes stop escalating and begin to cool.

- Breadth: fewer new lows; more stocks regain key levels.

- Credit: spreads stabilize or tighten.

- Price: the market begins making higher lows and holding rallies.

You don’t need all of them. But the more you have, the less you’re relying on vibes and hope.

Match the strategy to the kind of investor you are

If you’re a long-term investor

Your edge is not being a wizard. Your edge is time. Bottoms are notoriously hard to call,

and missing a handful of strong rebound days can hurt long-run returns. That’s why many long-term strategies focus on:

- consistent contributions (dollar-cost averaging),

- periodic rebalancing,

- maintaining diversification instead of chasing whichever asset is currently humiliating you the least.

In plain English: your job is to keep showing up, not to win a market-timing trophy no one actually awards.

If you’re an active investor or trader

Confirmation matters more than heroics. Many traders wait for:

- a break above a key moving average,

- a higher low after the first bounce,

- or improving breadth that supports the rally.

The goal is to reduce the odds you’re buying the “first bounce” in a continuing downtrend.

Use position sizing to stay sane

One practical compromise: instead of “all in” vs. “all out,” scale in.

You might allocate in chunksadding exposure as evidence improves. That way you participate if the low is in,

but you keep dry powder (and emotional stability) if it isn’t.

Common misconceptions about market bottoms

“The bottom happens when the news turns positive.”

Often, the market bottoms while the news still stinks. Markets price the change in expectations, not

the comfort of the present moment. By the time the headlines feel safe, prices may already be higher.

“A low P/E automatically means it’s the bottom.”

Valuation helps, but it’s not a timing tool. Earnings can fall, estimates can change, and “cheap” can get cheaper.

Think of valuation as a gravity argument for long-term returns, not a calendar invite for the exact day.

“If volatility is high, it must be the bottom.”

High volatility can occur near bottoms, but it can also hang around during ugly bear phases. The more useful tell

is often how volatility behaves on retests and after major news.

A quick, practical “bottom spotting” framework

If you want something you can actually do (without buying seventeen monitors), try this:

- Watch for selling exhaustion: do down days start failing to make meaningfully lower lows?

- Look under the hood: are fewer stocks making new lows? Is participation improving?

- Check the stress gauges: does volatility stop escalating? Do credit spreads stabilize?

- Demand confirmation: does the market hold gains for weeks, not hours?

- Act like a grown-up: scale in, rebalance, and avoid turning one data point into a religion.

This approach won’t make you perfect. But it can keep you from making the classic mistake:

buying because you’re desperate for the pain to stop, rather than because the market is actually changing character.

Investor experiences: what a bottom feels like in real life (about )

Even though every bear market has its own villaininflation, rates, recession fears, a crisis, a policy shockthe

emotional script is weirdly consistent. And recognizing that script can help you avoid decisions that feel good

today and haunt you later.

Experience #1: The “doomscroll bottom.”

People don’t usually wake up and say, “Today seems like a lovely day to sell at the lowest prices in months.”

It’s more like: you’ve watched losses stack up, you’re tired of explaining to yourself why you’re “fine,” and

one more ugly headline pushes you into a mood of “I don’t carejust make it stop.” This is when investors often

sell not because their plan changed, but because their nervous system did.

Experience #2: The relief rally that feels like a prank.

Then the market rips highersometimes on news that feels minor compared to all the bad stuff still happening.

If you sold near the lows, this is when you start bargaining: “Okay, I’ll buy back in after it drops again.”

The market may oblige… or it may not. That uncertainty is why scaling in can be emotionally and mathematically

helpful: it reduces the need to be exactly right on exactly the right day.

Experience #3: The retest that tests you.

A common bottoming drama is the retest. Prices drift back toward prior lows, and you feel like you’re reliving

the worst part of the movie. But the second act sometimes has a subtle difference: fewer stocks are collapsing,

volatility is less explosive, and the selling feels less frantic. If you’re tracking internals, the retest can

look more like “a final exam” than “another disaster.” If you’re not tracking internals, it just feels like

the market is messing with you personally.

Experience #4: The “meh” moment.

Here’s the least cinematic but most common feeling near major lows: apathy.

After months of stress, investors stop arguing about whether the market will bounce and start saying things like,

“I’m just going to ignore it.” Ironically, that’s often when markets begin to stabilizebecause the selling

pressure has already done much of its damage.

Experience #5: The new leadership surprise.

When a bottom turns into a real recovery, it often doesn’t start with the stocks you love the most.

Leadership can rotate into areas that were demolished, overlooked, or simply priced for disaster. Many investors

miss early recoveries because they’re waiting for the exact same favorites to lead again. A more flexible mindset

(“where is strength showing up now?”) tends to work better than nostalgia investing.

The big takeaway from these experiences: a bottom is rarely a confident, triumphant moment. It’s usually a messy,

frustrating transition from panic to exhaustion to cautious optimism. If you expect clarity, you’ll be tempted to

wait too long. If you accept uncertainty, you can build a process that doesn’t require perfection.

Conclusion

A stock market bottom isn’t a single signalit’s a behavior change. You’ll often see fear peak,

selling pressure fade, breadth improve, credit stress ease, and price action shift from relentless breakdowns to

higher lows and sustained rallies. You still won’t “know” it’s the bottom in real time. But you can recognize when

the odds are improvingand invest in a way that doesn’t depend on being a one-day genius.

Informational basis: investor education and market data concepts commonly discussed by major U.S. institutions and financial publishers.