Table of Contents >> Show >> Hide

- What “boring investing” actually means

- Why boring investing still wins

- The real engine: time, not excitement

- What boring investing can look like in practice

- Why exciting investing often disappoints

- Five habits that make boring investing work even better

- Common myths about boring investing

- Examples of boring investing doing its job

- What boring investing feels like in real life

- Conclusion: boring investing still works because human nature hasn’t changed

Let’s say the quiet part out loud: boring investing is not exciting dinner-party material. Nobody leans in when you say, “I buy low-cost index funds, keep contributing, rebalance once in a while, and then go do literally anything else.” There is no dramatic soundtrack. No heroic stock pick. No screenshot of a 247% gain from a company that makes robot dog vitamins.

And yet, boring investing still works.

In fact, its biggest strength may be that it looks almost too plain to brag about. Boring investing is built on habits that are repeatable, inexpensive, diversified, and emotionally survivable. It does not ask you to be a genius. It asks you to be consistent. That turns out to be a very good trade.

This article is about why simple, disciplined investing continues to beat flashy behavior for many long-term investors. It is educational, not personalized financial advice, but it is based on real-world investing principles that have stood up through booms, busts, bubbles, panics, and the annual tradition of somebody claiming “this time is different.”

What “boring investing” actually means

Boring investing is not about ignoring your money. It is about removing unnecessary drama from the process of building wealth. In practice, it usually means a few simple things done well:

- Using broad, diversified investments instead of betting heavily on a few winners

- Keeping costs low

- Contributing regularly, whether markets look cheerful or grumpy

- Matching risk to your time horizon and tolerance

- Rebalancing instead of chasing whatever just went up

- Staying invested for years, not headlines

That might sound underwhelming, but that is the point. Good investing often looks repetitive from the outside and powerful on the inside.

Why boring investing still wins

1. It focuses on the few things you can actually control

You cannot control what the market will do next month. You cannot control interest rates, election headlines, global conflicts, meme-stock stampedes, or the neighbor who suddenly thinks he is Warren Buffett because he bought one semiconductor stock at the right time.

You can control your savings rate, your asset allocation, your diversification, your fees, and your behavior. That matters because investing success is often less about prediction and more about process.

Low-cost investing is especially important because fees do not merely nibble at returns. They compound in reverse. If your portfolio grows over decades, even a seemingly small difference in annual expenses can create a very large gap in what you keep. That is one reason boring investors tend to be almost suspiciously interested in expense ratios. It is not because they are dull. It is because math has no mercy.

2. Diversification is not flashy, but it is useful

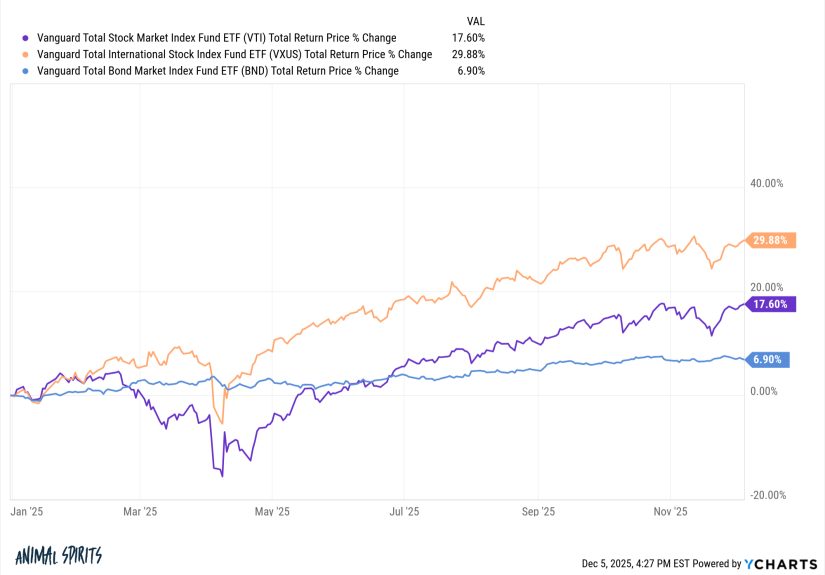

A concentrated portfolio can feel brilliant right up until it feels terrible. Owning a broad mix of stocks, bonds, and sometimes international exposure will not make you look like a market wizard in every season. It will, however, reduce the chance that one bad bet wrecks your plan.

Diversification works because markets do not move in perfect sync. Different assets respond differently to inflation, recessions, rate changes, and growth scares. A diversified portfolio does not eliminate losses. Nothing honest can promise that. But it can make the ride less violent and help keep you invested long enough to benefit from recovery.

In other words, diversification is the vegetable of investing. Not thrilling, very necessary.

3. Boring investing lowers the odds of self-sabotage

Many investing mistakes are behavioral, not mathematical. Investors get impatient in slow markets, euphoric in hot markets, and terrified in falling markets. That is how people end up buying things after big runs and selling them after big drops, which is a neat little trick for turning volatility into regret.

Boring investing creates guardrails. Automatic contributions, recurring purchases, and a simple asset mix reduce the number of emotional decisions you have to make. That matters more than most people realize. A decent plan followed consistently often beats a clever plan abandoned at the worst possible moment.

4. The “beat the market” dream is harder than it looks

There will always be stories about investors who outperformed by owning the right stock at the right time. Those stories are real. So are lottery winners. The problem is turning those stories into a reliable long-term strategy.

Across many time periods, a large share of actively managed funds fail to beat their benchmark after costs. That does not mean active management never works. It means it is hard, inconsistent, and often more expensive. Once you add fees, taxes, turnover, and plain old bad timing, the gap between theory and reality gets wider.

This is one reason index investing remains so appealing. You are not trying to identify the next superstar manager, guess when to rotate sectors, or forecast what the Federal Reserve will do three Tuesdays from now. You are buying broad market exposure, keeping costs down, and letting time do much of the heavy lifting.

The real engine: time, not excitement

Boring investing works because compounding rewards patience. The longer you leave a sensible portfolio alone and continue adding to it, the more your returns begin generating returns of their own.

This is where many people get tripped up. They think good investing should feel productive all the time. They want movement. Action. Buttons. Alerts. A sense that they are doing something.

But long-term investing is not improved by constant fiddling. In many cases, the most productive move is continuing the plan while resisting the urge to turn every market wobble into a personal emergency.

That is one reason automatic investing is so powerful. When money goes into the market on a regular schedule, you buy in good times and bad times alike. You do not need perfect timing. You need a functioning calendar and enough self-control not to interrupt it every time financial news gets theatrical.

What boring investing can look like in practice

A boring portfolio does not have to be identical for everyone. Age, goals, income stability, time horizon, and risk tolerance all matter. But the structure is often surprisingly simple.

Option 1: The ultra-simple route

Some investors use a target-date retirement fund. That approach bundles diversification and automatic rebalancing into one product. It is designed to become more conservative over time, which can make it appealing for people who want a very hands-off process.

Option 2: The basic fund mix

Others use a small set of broad funds, such as:

- A total U.S. stock market fund or S&P 500 fund

- An international stock fund

- A bond fund, depending on goals and risk tolerance

That is not glamorous. It also happens to cover a huge amount of the investable world without requiring you to become a part-time economist.

Option 3: The workplace autopilot route

For many people, the most effective boring strategy starts inside a 401(k) or similar retirement plan. Contributions come directly from each paycheck, reducing the temptation to spend first and invest “later,” which is a finance phrase that often means “never.”

Tax-advantaged accounts can make boring investing even more useful because they help shield growth from unnecessary tax drag, depending on the account type and the investor’s situation.

Why exciting investing often disappoints

Exciting investing usually comes packaged with one or more of the following:

- Higher costs

- More trading

- Greater concentration risk

- More taxes in taxable accounts

- A stronger urge to check the market every nine minutes

- A higher probability of making decisions for emotional reasons

Excitement can feel like intelligence because it creates motion. But activity and effectiveness are not the same thing. A lot of portfolios get busier without getting better.

Think about the classic cycle. A hot area of the market takes off. Investors pile in after the headlines. Prices rise further. Confidence turns into storytelling. Then momentum cools, reality returns, and the same investors who arrived late start looking for the exit. The investment did not just fail them. Their behavior helped fail them too.

Boring investing does not promise immunity from downturns. It simply avoids building a strategy around adrenaline.

Five habits that make boring investing work even better

1. Automate contributions

Automation removes guesswork and hesitation. It turns investing into a routine expense, like a bill you pay to your future self.

2. Keep fees ruthlessly low

You may not know next year’s best-performing fund. You can know whether you are paying too much.

3. Rebalance occasionally

Rebalancing helps keep your risk profile from drifting too far. It forces a little discipline by trimming what has run hot and adding to what has lagged.

4. Leave room for cash reserves

An emergency fund helps you avoid selling long-term investments at lousy times just to cover short-term problems. That cash buffer is not boring in a bad way. It is boring in a “thank goodness I had this” way.

5. Measure progress by goals, not gossip

The benchmark for success is not whether your cousin’s friend doubled money on a stock you had never heard of. It is whether your plan is moving you toward your own goals.

Common myths about boring investing

“It’s too simple to work.”

Simple does not mean weak. Simple means fewer moving parts, fewer opportunities for mistakes, and a clearer link between behavior and results.

“I’m leaving money on the table if I don’t chase big winners.”

You may miss some spectacular winners. You also avoid many spectacular losers. Broad exposure means you still participate in market growth without needing clairvoyance.

“I should wait until the market feels safer.”

Markets rarely send engraved invitations that say, “All clear now.” Waiting for perfect comfort can turn into a long-standing hobby with terrible returns.

“Bonds, cash reserves, and rebalancing just slow me down.”

Sometimes they do limit upside in roaring markets. They also help manage risk and protect behavior. A strategy only counts if you can stick with it in real life.

Examples of boring investing doing its job

Consider two imaginary investors.

Investor A chases trends. In one year it is AI stocks, then tiny biotech names, then options, then “just a little leverage,” then a sudden vow to hold only cash after a bad quarter. The portfolio is exciting, conversation-ready, and deeply vulnerable to mood swings.

Investor B uses a diversified mix of low-cost funds, contributes every month, rebalances once or twice a year, and mostly ignores market noise. The portfolio is so boring it could be mistaken for office furniture.

Investor A may occasionally have a spectacular year. Investor B is more likely to have a durable process. Over long stretches, durable processes have a habit of looking smarter than thrilling impulses.

That is the dirty secret of wealth building: it is often less cinematic than people hoped.

What boring investing feels like in real life

Here is the part people do not always say out loud: boring investing can feel emotionally awkward even when it is working.

It feels awkward when your coworker is talking about a stock that doubled and your total market fund is just quietly being a total market fund. It feels awkward when financial news turns every market dip into a breaking event with dramatic music and deeply concerned eyebrows. It feels awkward when your account is down and your plan tells you to keep contributing anyway. Human beings are not naturally built to enjoy buying things that just got cheaper if those things are stocks instead of sneakers.

It also feels strangely uneventful in good markets. There is no masterstroke to celebrate. No cinematic moment where you pound the desk and yell, “I knew it!” Your money grows, but the process stays ordinary. Contributions go in. Dividends get reinvested. Asset allocation drifts a bit. You rebalance. Repeat until retirement or until you become the kind of person who gets weirdly excited about tax efficiency.

Many experienced investors eventually realize that this emotional dullness is a feature, not a bug. The less your strategy depends on frequent decisions, the less opportunity you have to sabotage it. A portfolio that does not constantly tempt you into heroics is often a portfolio that survives you.

There is also a very practical kind of relief that comes with boring investing. You spend less time hunting for the next winner. You spend less energy regretting the last loser. You stop treating every market move like a referendum on your intelligence. Your money has a job. You have a process. Life gets some of its bandwidth back.

That does not mean boredom is effortless. During rough markets, the boring plan can feel almost offensively calm. Rebalancing into a falling asset class feels backward. Continuing automatic contributions during volatility can feel like walking into the rain on purpose. Holding a diversified portfolio while one hot sector dominates headlines can make you feel like the only person at the party drinking water.

But then markets change, leadership rotates, excitement cools, and the old virtues start looking attractive again. The investors who stayed diversified may not have won every sprint, but they gave themselves a real chance in the marathon. They preserved a habit, not just a position.

That is the experience many long-term investors eventually describe. Boring investing does not make them feel brilliant every month. It makes them feel organized, less reactive, and surprisingly free. Over time, that freedom matters. You are not glued to a screen. You are not rebuilding your strategy every season. You are simply letting a sensible system do what it was designed to do.

And yes, that sounds boring. It also sounds a lot like progress.

Conclusion: boring investing still works because human nature hasn’t changed

The tools may evolve. Markets may get faster. News may get louder. Apps may make trading look like a video game designed by caffeinated confetti enthusiasts. But the core truths of investing remain stubbornly familiar.

Costs matter. Diversification matters. Behavior matters. Time matters. The urge to chase, panic, predict, and overreact still causes trouble. That is why boring investing still works. It is not outdated. It is durable.

If your goal is long-term wealth building rather than short-term entertainment, boring may be exactly what you want. Not because it is thrilling, but because it keeps more of the market’s return, reduces avoidable mistakes, and gives compounding enough time to get to work.

So no, boring investing is not glamorous. It will probably never trend for the right reasons. But it has one deeply annoying quality that flashy strategies often lack: it keeps showing up and doing the job.