Table of Contents >> Show >> Hide

- Why the Market Keeps Hitting New Highs (Even When It Feels Suspicious)

- What History Says About Buying at All-Time Highs

- The Real Risk Isn’t the All-Time HighIt’s Your Time Horizon

- A Smart Playbook for Investing When Stocks Are at Highs

- Common Mistakes Investors Make at Market Highs

- When It Might Make Sense to Slow Down (Without Panic)

- Conclusion: Invest Like the Market Will Surprise You (Because It Will)

- Investor Experiences: What It Feels Like to Buy at the “Top” (and Keep Going)

- SEO Tags

You know that feeling when you finally decide to buy something… and the price is the highest it has ever been?

Like concert tickets, eggs, or that one hoodie your friend swears is “limited edition.” Investing at an all-time high

can feel like you’re walking into a party right when someone shouts, “Last call!” and you’re holding a tray of

expensive snacks.

But here’s the twist: in the stock market, “all-time highs” aren’t a rare cosmic event. They’re part of the design.

Markets that grow over time are supposed to make new highs. The real question isn’t “Is this a top?”

It’s “Do I have a plan that works even if this isn’t the top… and also works if it is?”

This article breaks down what all-time highs really mean, what history suggests (without pretending the future is a

rerun), and how to invest intelligently when the headlines scream “RECORD!” like they’re trying to sell you a used

car.

Why the Market Keeps Hitting New Highs (Even When It Feels Suspicious)

A stock index reaching an all-time high sounds dramatic, but it’s often just the natural outcome of long-term growth.

Over time, companies sell more stuff, raise prices, innovate, expand into new markets, and (ideally) become more

profitable. Add inflation (which can push revenue numbers higher in dollar terms) and population/productivity growth,

and you get a market that tends to drift upward over long periodsoften in a messy, zigzag way.

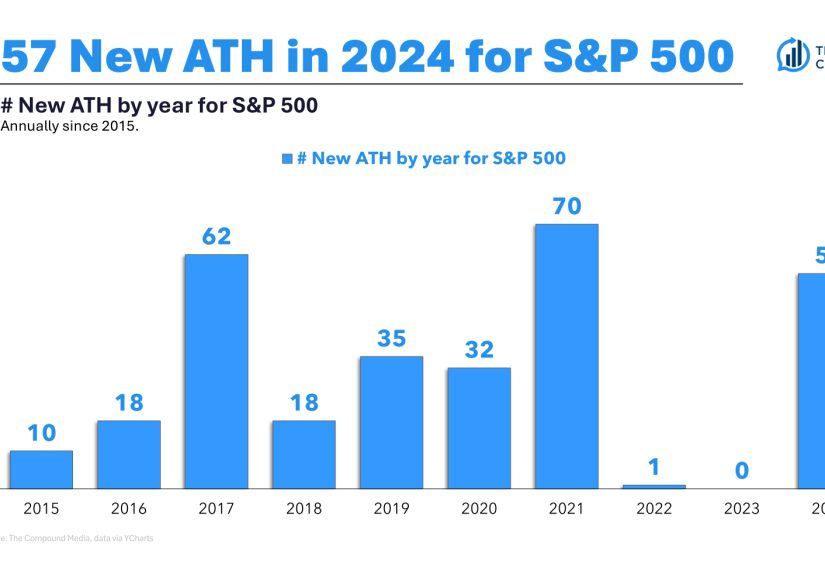

All-time highs are often clustered, not isolated

New highs frequently come in batches. When the economy is resilient, earnings are strong, and investor confidence is

decent, markets can make repeated highs close together. That’s why “waiting for a pullback” can sometimes turn into

“waiting forever,” or at least waiting long enough to miss meaningful gains.

Indexes evolve over time

Major indexes aren’t museums; they’re living collections. Companies rise, fall, merge, get replaced, or shrink in

importance. That evolution can help indexes reflect the parts of the economy that are growing (technology has been a

big example in recent decades). This doesn’t guarantee smooth returns, but it helps explain why long-term charts tend

to lean upward.

What History Says About Buying at All-Time Highs

If investing at a record high were automatically a mistake, long-term investors would be doomedbecause record highs

happen regularly. Some analyses note that since 1950 the S&P 500 has hit all-time highs on a meaningful share of

trading days, and many of those highs eventually become “floors” you never see again. Translation: sometimes there

is no “better entry,” just a different entry.

Record highs don’t reliably signal an immediate crash

A common fear is that an all-time high is like the peak of a roller coaster, and the only direction left is down.

But markets don’t work like gravity. They work like a weird mix of business performance, expectations, interest

rates, global events, and human emotions (which are famously calm and rational, as we all know).

Several market commentaries from major investment firms have found that average returns after record highs have often

been similar to (and sometimes slightly better than) returns after random daysespecially over shorter horizons.

That’s not a promise. It’s a reminder that “high” isn’t the same as “done.”

But “high” can matter more over longer time horizons

Here’s the nuance people skip when they’re busy arguing online: valuation can influence long-term expected returns.

If you buy when prices are high relative to fundamentals (like earnings), your long-run returns may be lower than if

you bought when prices were cheaper. Some research notes that while markets can do fine after hitting all-time highs

in the short-to-intermediate term, longer-term forward returns (think 10+ years) can lag compared to starting points

that weren’t at record levels.

The practical takeaway is not “never invest at highs.” It’s: don’t let the price level replace your plan.

If your plan depends on perfectly avoiding high prices forever, your plan is basically fan fiction.

A reality check using a simple example

Imagine two investors, Alex and Jordan.

- Alex waits for a “meaningful correction” before investing.

- Jordan invests steadily each month into a diversified portfolio.

If a correction happens quickly, Alex might feel brilliant. If it doesn’t, Alex may stay in cash while the market

keeps climbing, and then either (1) buys even higher later, or (2) never buys at all. Jordan isn’t trying to be

brilliant. Jordan is trying to be consistent. Over a long horizon, consistency can beat brillianceespecially the

kind that only exists in hindsight.

The Real Risk Isn’t the All-Time HighIt’s Your Time Horizon

One of the most underrated investing truths is that the same market level can be “fine” for one person and “a terrible

idea” for another, depending on when they’ll need the money.

If you need the money soon, stocks may be the wrong tool

If you’re investing cash you’ll need in the next 1–3 years (tuition, rent, a car, an emergency fund, a short-term

goal), the issue isn’t whether the market is at a high. The issue is that stocks can drop sharply at any timeand

“sharp” is not a flavor you want in your rent money.

If your horizon is long, volatility becomes a fee you pay for growth

Over longer periods, market declines are still unpleasant, but they’re less likely to permanently derail a plan

especially if you’re diversified, keep costs low, and avoid panic decisions.

A Smart Playbook for Investing When Stocks Are at Highs

1) Start with asset allocation, not headlines

Asset allocation is the mix of stocks, bonds, and cash that fits your goals and risk tolerance. It’s the “boring”

part of investing that quietly does most of the heavy lifting. A diversified allocation can reduce the odds that one

bad year (or one overhyped sector) wrecks your whole situation.

If you’re not sure where to start, a broad guideline is:

keep emergency cash separate, invest long-term money in a diversified portfolio, and match risk to your timeline.

(If you’re investing as a teen, loop in a parent/guardian or a trusted adultespecially for account setup,

taxes, and risk decisions.)

2) Use dollar-cost averaging to reduce “timing regret”

Dollar-cost averaging (DCA) is investing a fixed amount at regular intervals, regardless of market level. When prices

are high, you buy fewer shares. When prices drop, you buy more. The goal isn’t to “beat the market” with a trick.

It’s to reduce the emotional stress of picking the perfect daybecause perfect days are shy and avoid eye contact.

DCA can be especially useful if you’re nervous about investing a lump sum at an all-time high. Automating

contributions (like through a retirement plan) turns investing into a habit instead of a monthly debate with your

own anxiety.

3) Lump sum vs. DCA: choose the strategy you can stick with

Historically, lump-sum investing often outperforms DCA because markets trend upward more often than downward, so money

invested sooner has more time to compound. But DCA can be a strong “behavioral advantage” if it keeps you from

freezing, delaying, or dumping everything after the first scary headline.

If you’re sitting on cash and unsure, one practical compromise is “planned DCA”:

pick a timeline (like 3–12 months), automate the schedule, and commit to it. No “pause button” just because the

market had a dramatic day and your group chat started quoting doom memes.

4) Rebalance so winners don’t quietly hijack your risk

When markets rise, certain holdings can grow so much that your portfolio becomes more aggressive than you intended.

Rebalancing means trimming what’s grown beyond your target and adding to what’s laggedbringing the portfolio back

to your planned mix. It’s a disciplined way to avoid accidental overexposure to whatever has been hottest lately.

5) Focus on what you control: fees, diversification, behavior

You can’t control whether the market is at a high. You can control:

- Using diversified, broad-market funds instead of chasing a single stock or theme

- Keeping costs low (fees matter more than most people admit)

- Staying consistent through volatility

- Not investing money you’ll need soon

- Having a clear reason for every investment decision (not just vibes)

Common Mistakes Investors Make at Market Highs

Waiting for “the dip” that never arrives

Corrections do happen. But markets don’t schedule them around your calendar. Waiting can become a long-term strategy

of doing nothing, which is surprisingly effective at producing exactly zero compounded returns.

Letting FOMO pick your investments

When markets hit new highs, hype is loud. The danger is chasing whatever just went up the most, without understanding

valuation, business fundamentals, or your own risk tolerance. If the only reason you’re buying is “everyone’s talking

about it,” you’re not investingyou’re auditioning for a cautionary tale.

Ignoring concentration risk

A rising market can become narrow, driven by a small group of huge stocks. That can make index returns look calm

while the average stock is less impressive. Diversification helps, but it’s also a reminder to understand what you

actually own (especially if you’re all-in on one sector fund or a handful of names).

Checking prices too often

If you measure your long-term plan with a 15-minute ruler, you’ll feel emotional whiplash. Over-monitoring can lead

to overreacting. Investing is one of the few activities where “doing less” can be a genuine advantage.

When It Might Make Sense to Slow Down (Without Panic)

“Don’t freak out” doesn’t mean “ignore reality.” Even at all-time highs, there are sensible reasons to adjustbased

on your situation, not the market’s mood.

- You don’t have an emergency fund. Build that first before taking market risk with money you might need.

- You have a near-term goal. If you need the money soon, reduce stock exposure regardless of highs.

- Your portfolio is riskier than you can tolerate. If a normal downturn would make you panic-sell, rebalance now.

- You’re carrying high-interest debt. Paying that down can be a “guaranteed return” that’s hard to beat.

Notice what’s missing: “The market is at a high” is not on the list by itself. It’s context, not a command.

Conclusion: Invest Like the Market Will Surprise You (Because It Will)

Investing at all-time highs can feel like stepping onto a moving treadmill: you worry it’s about to speed up,

trip you, and launch you into the emotional stratosphere. But long-term investing isn’t about avoiding every

uncomfortable moment. It’s about building a process that works across uncomfortable moments.

Markets can fall after hitting highs. They can also rise for years after hitting highs. The people who tend to do

better aren’t the ones who perfectly predict the next dip. They’re the ones who diversify, control costs, invest

consistently, and don’t let fear or hype drive the steering wheel.

Educational note: This article is for general information, not personalized financial advice. If you’re new to

investing (especially if you’re a teen), consider learning with a trusted adult and using simple, diversified

approaches until you understand risks, fees, and taxes.

Investor Experiences: What It Feels Like to Buy at the “Top” (and Keep Going)

Let’s talk about the part nobody puts in a chart: the feelings. Investing at an all-time high isn’t just a math

decision; it’s a psychology decision. And psychology has a habit of showing up uninvited, eating your snacks, and

changing the playlist.

Experience #1: The “I bought and it immediately dropped” moment.

Many investors have a story where they finally investedthen the market dipped within days or weeks. It feels

personal, like the market waited for you specifically. The lesson most people learn (eventually) is that short-term

drops are normal. What matters is what you do next. The investors who do best tend to keep investing through the

drop (especially via automatic contributions), rather than retreating to cash out of embarrassment.

Experience #2: The “I waited for a dip and the dip never came” regret.

Another common story: an investor parks cash because the market is “too high.” Weeks become months. The market rises.

The investor keeps waiting. Eventually, they buy at an even higher levelor they give up and stay on the sidelines.

The emotional pattern is sneaky: waiting feels safe, but it can quietly become costly. People who escape this cycle

usually switch from “decision-based investing” to “system-based investing,” like monthly automatic purchases.

Experience #3: The 401(k) investor who barely noticed the highs.

Investors who contribute through a workplace plan often report a different experience: they didn’t time anything.

Money went in automatically every paycheck. During market highs, they bought fewer shares; during downturns, they

bought more. Over time, their cost basis smoothed out. The big benefit wasn’t superior predictionit was reduced

temptation to overreact. Automation can be an underrated superpower.

Experience #4: Living through a real crash changes your definition of “high.”

Investors who lived through 2000–2002 (dot-com bust), 2008–2009 (global financial crisis), or the sharp 2020 pandemic

drop often describe the same shift: they stopped believing there’s a “safe price” and started focusing on “safe

behavior.” Some learned to keep more cash for emergencies. Others learned to diversify better. Many learned that

selling during panic feels like relief in the moment and regret later. The market’s recovery timeline can be

unpredictable, but the emotional script is surprisingly repetitive.

Experience #5: Rebalancing feels weirduntil it saves you.

People who rebalance in a rising market often say it feels like trimming a winner “too early.” But when a concentrated

bet later cools off, they’re glad they reduced risk while things were strong. Rebalancing is one of those habits that

looks boring during good times and looks genius only after the factwhich is exactly why it works as a discipline.

Experience #6: The best strategy is the one you can repeat when you’re nervous.

A big takeaway investors often share is that the “optimal” strategy on paper isn’t always optimal in real life. If

lump-sum investing makes someone so anxious that they abandon the market at the first downturn, then the real-world

result may be worse than a calmer, consistent approach. That’s why some investors prefer a structured planlike

investing a lump sum in thirds over a few monthsbecause it’s easier to follow through without improvising.

If there’s a common thread across these experiences, it’s this: investing success is often less about avoiding all-time

highs and more about avoiding all-time bad decisionspanic selling, FOMO buying, and abandoning a plan when the market

does what markets always do: surprise everyone.