Table of Contents >> Show >> Hide

- Quick takeaways (for people who like receipts, not speeches)

- What counts as a bear marketand why “new highs” matter

- How markets climb from “bear” to “brand-new high”

- Real-world examples: when new highs returned (and how long it took)

- The “new high” anxiety is real (and very common)

- How to approach new all-time highs without trying to time the market

- Myths about all-time highs after a bear market (let’s retire these)

- What to watch (and what to ignore) when markets hit new highs

- FAQs: New all-time highs after a bear market

- Investor experiences: what “new highs after a bear market” feels like (the human version)

- Conclusion: The point of new highs isn’t perfectionit’s progress

If you’ve ever watched the stock market crawl out of a bear market and hit brand-new all-time highs, you’ve probably felt two emotions at once:

relief (“We survived!”) and suspicion (“Okay… but is this a trap?”). Congratsyour brain is working exactly as designed.

Unfortunately, your brain was designed for avoiding saber-toothed tigers, not for calmly dollar-cost averaging while financial headlines scream in ALL CAPS.

The good news: new highs after a bear market are not a glitch in the systemthey’re a feature of how markets historically recover, re-price risk,

and move forward. The tricky part is that the road to those highs can feel like driving with a “CHECK ENGINE” light on… for months.

Quick takeaways (for people who like receipts, not speeches)

- Bear markets endoften before the news cycle admits it.

- New all-time highs are normal in an upward-trending market, even if they feel “too high.”

- Recoveries vary: some take months, others take years, depending on what caused the bear market.

- The biggest risk is behavioral: panic-selling near lows and waiting “for certainty” near the rebound.

What counts as a bear marketand why “new highs” matter

A bear market is commonly defined as a major index falling at least 20% from a recent peak. That definition is simple on purpose:

it’s a quick way to describe a big sentiment shiftfrom “stocks only go up” to “I’m never checking my account again.”

All-time highs aren’t just bragging rights

“All-time high” is the market’s way of saying: the price has surpassed every previous closing level in history.

That matters because it’s a psychological reset. Investors who bought at the prior peak are finally back in the green, and the market’s narrative

shifts from “recovery” to “expansion.” It’s also a reminder of a basic truth: markets don’t need to “get back to normal”they create a new normal.

Why all-time highs happen more often than people think

A common misconception is that all-time highs are rare unicorn sightings. In reality, because markets have historically trended upward over long periods,

they can spend a meaningful amount of time making new highs. One major market research note: since 1950, the S&P 500 has reached an all-time high on

roughly about 7% of trading daysand many of those highs later became “floors” investors never got to buy below again.

How markets climb from “bear” to “brand-new high”

Recoveries often look messy in real time. That’s because the market is forward-looking: it tries to price the next 6–18 months of expectations

while the present moment is still wearing sweatpants and anxiety.

1) The math of recovery is weird (but helpful)

If an index falls 20%, it doesn’t need +20% to break evenit needs +25%. If it falls 50%, it needs +100%. This is why the early part of a rebound

can feel fast: once selling pressure fades and buyers return, gains can compound quickly off a lower base.

2) Sentiment turns before headlines

Markets tend to bottom when fear is loud, forecasts are gloomy, and everyone suddenly becomes an expert in doom. Often, the shift happens quietly:

inflation cools, job losses aren’t as bad as expected, earnings stop falling, or the central bank signals a pause. The headlines usually catch up later.

3) Liquidity and policy can matter (a lot)

Some bear markets are “event-driven” (a shock), others are “cyclical” (tied to the economy), and some are “structural” (financial system stress).

The recovery speed often depends on what brokeand how fast it gets repaired.

Translation: a one-time shock can rebound faster than a balance-sheet crisis. One is a sprained ankle. The other is reconstructive surgery.

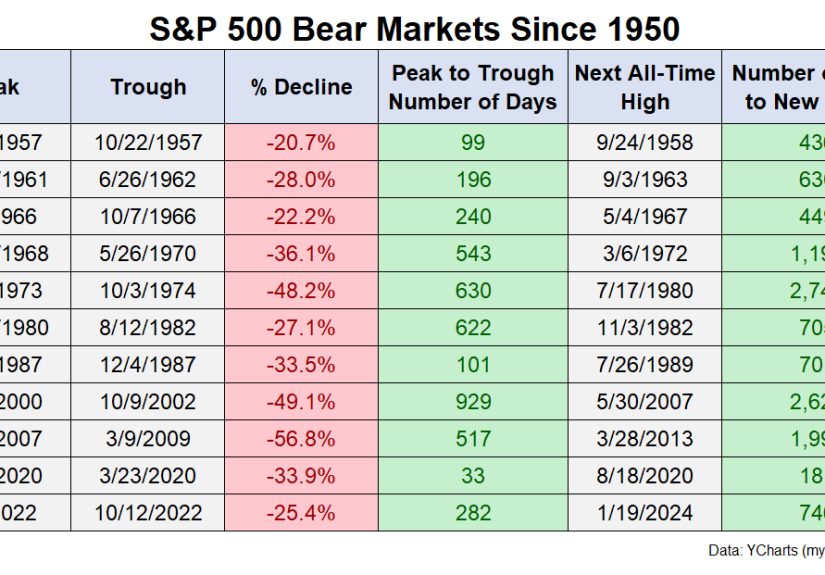

Real-world examples: when new highs returned (and how long it took)

Here are a few well-known U.S. stock market examples that show why “new all-time highs after a bear market” can mean very different timelines.

(And yes, your feelings during each timeline are also different. In a long recovery, the dominant emotion is usually “Are we there yet?”)

Example A: The 2020 pandemic drop (fast recovery)

In early 2020, the S&P 500 dropped sharply during the COVID-19 shockthen recovered rapidly. The index ultimately closed above its pre-pandemic record

later that year, marking a historically quick round-trip.

Example B: The 2007–2009 financial crisis (slow, then steady)

The Global Financial Crisis was a deeper, system-level stress event. U.S. stocks fell hard, then began a long climb. It took yearsnot monthsfor the

market to surpass its prior record closing level and set a new high. This is the classic “rebuild confidence” recovery: slow, frustrating, and then

suddenly you look back and realize the distance covered.

Example C: The 2022 bear market (middle-speed recovery)

The 2022 drawdown was driven by inflation, rising interest rates, and a broad valuation reset. When inflation data began to cool and earnings held up

better than feared, the market stabilized and eventually returned to record territory the following year.

So what’s “normal”?

Historically, bear markets have often been shorter than bull markets. Some long-term studies summarizing U.S. equity history estimate the average

bear market duration around monthsnot yearsthough the range is wide. The time to regain prior peaks and push to new highs can also vary dramatically,

with deeper crises typically taking longer to fully recover.

The “new high” anxiety is real (and very common)

Here’s the emotional paradox: investors beg for the market to recover… and then feel nervous once it does. That’s not hypocrisyit’s psychology.

After a bear market, your brain is trained to scan for danger. So when prices rise, your brain says, “This looks suspiciously like happiness.

We should stop it.”

Common mental traps

- Recency bias: You overweight the most recent pain and underestimate the long-term trend.

- Anchoring: You fixate on the old peak and treat it like a “ceiling,” even though markets don’t have ceilings.

- Confirmation hunting: You only click articles that agree with your fear. (Your algorithm loves this.)

- “I’ll get back in when things feel safe”: Markets often feel safest after much of the rebound has already happened.

Wall Street has a phrase for this uneasy climb: markets can “climb a wall of worry.” That’s a poetic way of saying: the market doesn’t wait for everyone

to feel comfortable before it moves higher.

How to approach new all-time highs without trying to time the market

Nobody has a crystal ball. Even people who claim they do are usually just holding a snow globe and shaking it confidently.

What you can control is your process.

1) Use contributions, not predictions

If you’re investing for long-term goals, a steady contribution plan (often called dollar-cost averaging) can reduce the emotional load.

You’re not betting on one “perfect” day. You’re building a habit.

2) Rebalance like a grown-up (even when it’s boring)

After rebounds, portfolios can driftstocks may become a bigger slice than you intended. Rebalancing is the anti-drama move: it helps align your

portfolio with your risk tolerance rather than your latest adrenaline spike.

3) Keep your emergency fund separate

Bear markets hurt the most when you’re forced to sell at the wrong time. A cash buffer for near-term needs can help you avoid turning a temporary

drawdown into a permanent loss.

4) Make a “headline policy”

Decide in advance how you’ll respond to scary news. Example: “I will not make major portfolio changes based on one day of market movement.”

This is less glamorous than “timing the top,” but it tends to work better for real humans.

Myths about all-time highs after a bear market (let’s retire these)

Myth #1: “Buying at all-time highs is always bad.”

Markets often make new highs in strong long-term uptrends. If you only invest at “comfortable” prices, you may miss long stretches of compounding.

The better question is usually: Does my plan match my time horizon and risk tolerance?

Myth #2: “A bear market ends when the economy feels good again.”

The stock market and the economy are related but not identical. The market can rebound while economic data is still ugly, because investors are pricing

the future, not writing a diary about the present.

Myth #3: “If I wait for certainty, I’ll be safer.”

Certainty is expensive. By the time everything looks “safe,” prices may already reflect that improved outlook.

What to watch (and what to ignore) when markets hit new highs

Worth watching

- Earnings and guidance: Are companies holding up, improving, or deteriorating?

- Inflation and rates: Not because you need to forecast the Fed, but because rates influence valuations.

- Market breadth: Are gains concentrated in a few names, or is participation broadening?

Usually not worth watching

- “This time is different” hot takes that offer certainty with zero humility.

- One-week price moves masquerading as destiny.

- Influencer-level predictions delivered with the confidence of a weather app from 1997.

If you want one practical rule: match your decision timeframe to your goal timeframe.

Retirement decisions shouldn’t be made on a 48-hour news cycle.

FAQs: New all-time highs after a bear market

Does a new all-time high mean a crash is coming?

Not automatically. Markets can pull back from highs (sometimes sharply), but new highs can also be part of longer bull market cycles.

The presence of a new high is not, by itself, a reliable timing signal.

Why do the best days happen near the worst days?

Volatility clustersbig moves often happen in turbulent periods. This is one reason market timing is so difficult: stepping out “to be safe” can

accidentally mean missing powerful rebound days that materially affect long-term returns.

How do I reduce regret if I missed the bottom?

The bottom is obvious only in hindsight. A consistent planautomatic contributions, diversification, and periodic rebalancingcan help you move forward

without turning investing into a daily self-critique exercise.

What’s the biggest lesson from history?

Markets have historically recovered from bear markets and gone on to make new highs. The costliest mistakes tend to happen when investors let fear

override processselling near lows and waiting too long to re-engage.

Note: This article is educational and not individualized financial advice.

of experiences appended below

Investor experiences: what “new highs after a bear market” feels like (the human version)

The history books make recoveries look tidy. The lived experience is more like a group chat where half the people are panicking, a quarter are bragging,

and the remaining quarter are quietly rebalancing and refusing to make eye contact.

Experience #1: “I sold near the bottom… and now I’m waiting for a ‘better’ price.”

This is the most common emotional hangover after a bear market. An investor exits because the decline feels unbearable, promising themselves they’ll

“buy back in when things stabilize.” Then the market rebounds in uneven burstsup big one week, down the nextand “stabilize” becomes an ever-moving

goalpost. When the index finally approaches its old peak, the investor feels angry instead of relieved: “How is it back already?”

It’s not just fear of loss anymore; it’s fear of regret.

What often helps here is a shift from “perfect entry” to “repeatable behavior.” Many investors rebuild confidence by restarting with smaller,

scheduled purchasesweekly or monthlyso they’re not trying to solve the entire emotional puzzle in one trade. Instead of asking,

“Is today the day?” they ask, “What does my plan do this week?”

Experience #2: “I stayed invested, but I didn’t feel braveI felt nauseous.”

Staying invested through a bear market is rarely cinematic. It’s not usually a triumphal montage with inspirational music. It’s more like:

you check your account, sigh deeply, close the tab, and go fold laundry with unnecessary intensity.

Investors who make it through often describe a subtle turning point: the day the market stops making fresh lows. Nothing feels “good” yet.

Headlines are still negative. Friends are still confident a bigger drop is coming. But prices begin to form a base, and the narrative shifts from

“How bad will it get?” to “How bad does it still need to get?”

When new all-time highs finally arrive, the emotional payoff can be strangely muted. Instead of euphoria, many people feel cautious:

“After what we just lived through, I don’t trust calm.” That’s normal. It’s also why rules-based habitsrebalancing, automatic contributions, and

keeping short-term cash needs separatematter so much. They protect you from making your next decision based on the last scar.

Experience #3: “The rebound happened, but leadership changed.”

Another real experience: the market recovers, but the “winners” look different than before. After some bear markets, leadership rotatessometimes away

from growth to value, sometimes from mega-cap dominance to broader participation, sometimes from one sector theme to another. Investors who were

concentrated in a narrow slice of the market can feel left behind even during a rebound.

This is where diversification stops being a boring textbook concept and starts being emotional insurance. You’re less dependent on guessing which

sector gets the microphone next.

If there’s one universal experience, it’s this: the market’s “all clear” message usually arrives after the recovery is already underway.

New all-time highs are often the confirmation, not the beginning. The investors who do best over time are usually the ones who build a plan that works

even when their feelings don’t.